Your investment journey – why and how you should invest

Your investment journey – why and how you should invest

When it comes to securing your financial future, just saving alone may not be enough. In this article, we share why investing is important and how you can get started with as little as S$100 a month.

Part 1: Stretching your dollar – why you should invest

“To thine own self be true” – Hamlet, by William Shakespeare

Many of us look forward to when we have enough money to quit our day jobs and still be able to afford a comfortable life after that.

But before we start dreaming, let’s consider some cold, hard facts.

We may each have our own view of what a “comfortable life” means and what it costs. But whether it’s an occasional restaurant meal, commuting via taxis now and then or an annual holiday overseas – they all cost money. When added up, the final cost of such indulgences can be daunting.

Use our online OCBC Life Goals Retirement Calculator to determine your number for your desired lifestyle.

Someone who is 25 years old today and wishes to retire at age 60 with the above lifestyle will probably need to accumulate about $2.1 million by the time they retire1. This is no small sum, considering the amount is on top of our regular bills, mortgage payments and living expenses.

Faced with the unpleasant prospect of having to pay off huge bills at the end of each month, most of us would rather pack up our dreams and return our noses to the grindstone for a monthly pay cheque that we hope to stretch as much as possible.

However, being intimidated may not be the best approach to growing your wealth over the longer term.

The best way to grow your wealth is by investing.

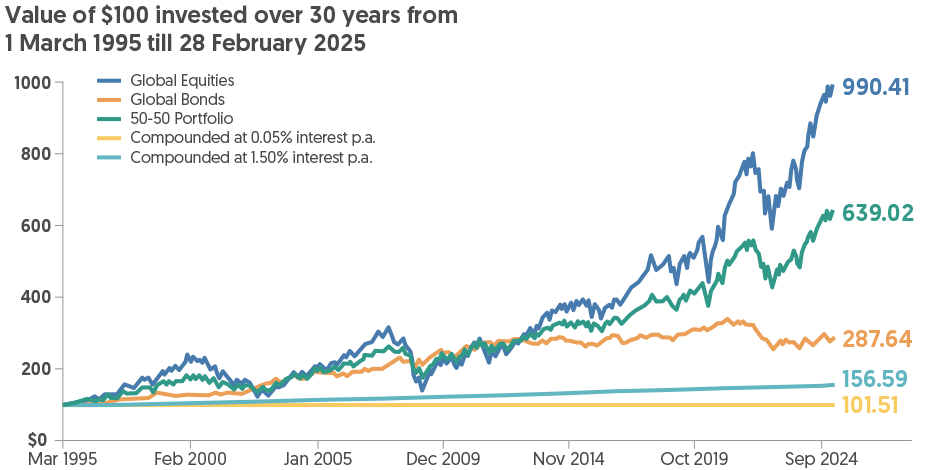

Putting aside some of your money into assets like unit trusts, stocks and bonds will have you realise your financial goals sooner as the expectation is that the value of these assets will increase at a faster rate over time than your savings account (Figure 1).

Figure 1: Investing in a diversified portfolio grows your money faster than keeping your money in a savings account and tends to be less volatile than just investing in equities or bonds alone.  Source: Bloomberg, as at 28 February 2025. Global Equities are represented by the MSCI World Index. Global Bonds are represented by the Bloomberg Barclays Global Aggregate Total Return Index. 50-50 Portfolio assumes a constant 50-50 allocation between Global Equities and Global Bonds. All dividends and coupons are assumed to be reinvested. “Compounded at 0.05% / 1.50% interest p.a.” assumes monthly compounding.

Source: Bloomberg, as at 28 February 2025. Global Equities are represented by the MSCI World Index. Global Bonds are represented by the Bloomberg Barclays Global Aggregate Total Return Index. 50-50 Portfolio assumes a constant 50-50 allocation between Global Equities and Global Bonds. All dividends and coupons are assumed to be reinvested. “Compounded at 0.05% / 1.50% interest p.a.” assumes monthly compounding.

Investing helps to mitigate the impact of inflation on your money. The cost of goods and services has been increasing – and will continue to do so – over the years, making things more expensive. This means that the dollar you hold today will be worth less in the future and the amount of goods you can buy with that dollar will be fewer due to the impact of inflation.

At OCBC Digital, we make your wealth journey so simple that you will wonder why you didn’t start sooner.

The only thing to fear is fear itself

For many of us, what is holding us back from investing is the perception that you need a large amount of money to get started.

On top of that, there is the perception that the journey to financial freedom would entail pain and sacrifice, which makes the process less enticing.

But the truth is, you only need a small amount of money to get started on investing. You can employ strategies like dollar cost averaging, whereby you invest a small amount of your salary (starting from as little as $100 per month) at monthly intervals into an investment of your choice.

Investing in this manner minimises risk. Plus, you remain invested regardless of which direction the market is going.

You can set up a monthly investment plan easily with our wide range of investment assets on OCBC Digital.

The journey begins one step at a time

Sometimes, we may get ahead of ourselves.

Before embarking on your first steps, you must first prepare yourself mentally for the journey ahead, particularly when it comes to understanding the concept of risk.

We can visualise risk as taking a long, winding but flat road to our destination or opting to cut through a jungle path to get there faster. But the terrain may be rough and there’s a greater chance of hidden surprises. There’s no right or wrong answer – it all depends on your personal preferences and situation.

Deciding how much and what kind of risk to take boils down to three factors: your Need, Ability and Willingness to take risks.

- Need to take risks

Stretching limited resources

We have many financial goals – retirement, children’s education, legacy planning, to name a few – but our resources (i.e. income) are limited. At the same time, inflation continues to erode the value of our savings over time. This means we need to target a certain rate of return to achieve our goals.

Deploying funds appropriately

Savings accounts, fixed deposits and endowments are a good start, but relying on them alone may not generate sufficient returns to meet your financial goals. The hard truth is that to achieve your goals, you may need to be prepared to take on some risks or set aside more money to invest over time through forced savings or even both.

Diversifying your investment portfolio using a combination of equities, bonds and other asset classes can improve your investment returns while lowering the risks than if you had put everything in one basket.

- Ability to take risks

Know your constraints

Your commitments, liabilities and disposable income determine the amount of loss you can afford to bear, and therefore your ability to take risks. The higher your commitments and liabilities, and/or the lower your disposable income, the lower your ability to take risks. This can be determined by analysing your yearly cash flow.

- Willingness to take risks

- Your willingness to take risk is determined by your personal preferences and is the most subjective of the three factors. This is usually determined via a risk profiling questionnaire which you should answer truthfully.

- Taking on too much risk is usually driven by setting high aspirations for your financial goals, but this can also mean a higher likelihood of negative returns – even enough to cause you to fall short of your financial goals. You can reduce this possibility by engaging an independent party, like a financial adviser, to assess and recommend investing decisions objectively.

- Taking on too little risk is typically due to a fear of losses and/or a lack of familiarity with the investments themselves. One way to overcome this is to learn more about the various ways and assets to invest in. Familiarity with how various investments generate returns and/or losses can help you by reducing the unknowns (which we will cover in part 2 below).

Assign a Low/Medium/High rating for each of the factors above (i.e. Need, Ability and Willingness). Understand your overall approach towards taking risks. For example, if your Need and Willingness are High but your Ability is Low, then your approach should be towards Lower Risk.

Why is this important? Staying the course is crucial in your investment journey and this can only be done when your Need, Ability and Willingness are aligned. You do not want to place yourself in a situation where you become disproportionately affected by sudden drops in market prices and thus bail out of your investments at an inopportune time. Only then will you be ready to begin your investing journey.

“Knowing yourself is the beginning of all wisdom” – Aristotle

Part 2: Hitting the road – how can you invest?

We’ve discussed the various asset classes that you can invest in our other article. The next step in your investing journey is to understand the various ways you can invest in these asset classes.

- Investing directly in equities and fixed income

Benefits

- Huge investment universe: Investing directly gives you access to a wide universe of securities. Investors can easily open accounts to invest directly in equity and fixed-income instruments, both locally and abroad.

- Higher return potential: Picking the right stocks and/or bonds can result in substantial gains relative to the broader market.

Potential snags

- Selection: Success in investing directly depends on your ability to pick the right instruments at the right time. This often requires time spent doing research to identify the best instruments.

- Larger minimum outlay, higher concentration risk: Certain equity markets and many bonds require larger initial investment amounts. This means you are more likely to place more of your eggs in the same basket, thus exposing your portfolio to concentration risk.

- More risk factors to manage: Investing in a smaller number of securities also means you have to bear more company-specific risks in addition to broader market risks.

- Investing in a bundle – Unit Trusts, Exchange Traded Funds (ETFs) and Real Estate Investment Trusts (REITs)

Benefits

- Convenience: You only need to perform one transaction to buy into or sell out of one fund. The fund manager will execute the buying and selling of all the securities within the basket. Most funds are easily accessible to individual investors.

- Diversification: You will be invested in a selected basket of securities which reduces company-specific, sector-specific and even country/region risks. This offers built-in protection if some of the fund investments decline in value.

- Economies of scale: Because a fund’s assets are pooled together from many investors, it can invest in certain assets or take larger positions than a small investor can.

Figure 2: Exchange Traded Funds (ETFs)

- An exchange traded fund (ETF) is a collection of tens, hundreds, or sometimes thousands of stocks or bonds in a single fund. These underlying securities are traded on stock exchanges. ETFs seek to replicate the returns of a market.

- ETFs are generally accepted to be an inexpensive, transparent and convenient way to get access to many different asset classes.

- Investors immediately access a very diversified portfolio of pre-selected securities on the cheap. If a single stock or bond in the collection is performing poorly, there's a good chance that another is performing well, which helps minimise losses.

- This makes it easy to diversify a portfolio and it also makes ETFs simple to buy and sell.

Source: OCBC Wealth Management

Potential snags

- Fees can reduce portfolio returns: If the fund does generate enough additional returns to offset its fees, your portfolio can underperform the benchmark index.

- Choosing managers, not securities: Choosing the right manager plays an important part in the success of your portfolio. The manager decides what and how to buy or sell within the fund. Therefore, you need to be comfortable with the manager’s decision-making.

- Potentially lower returns than investing directly: A diversified basket of securities spreads out the risks, but also spreads out the returns. The reduction in risk from diversification can result in potentially lower, but less volatile returns.

- Structured products – structured investments and dual currency investments

Benefits

- Benefiting from the underlying asset without having to own it: Structured investments offer potential returns that are higher than interest rates on traditional deposits and may even offer the potential for capital appreciation without having to own the underlying asset.

- Versatile: Structured investments allow you to tap into many different asset classes, such as equities, interest rates, fixed-income products, foreign exchange rates and even commodity prices.

- Customisable: You can mix the basket of underlying assets and even opt to include defensive features into your structured investments at the expense of some returns.

Potential snags

- High complexity: Structured products are complex financial instruments and require a thorough understanding for investors to appreciate the risks involved.

- Lack of liquidity: Structured products are not publicly traded and thus illiquid. Unwinding a structured product midway usually involves an unwinding cost.

- Counterparty risk: The failure of the issuer to meet its obligations may be passed on directly to the investor, exposing to the risks posed by the issuer as well.

- Insurance plans – Investment-Linked Life Insurance Plans (ILPs)

Benefits

- Dual purpose: You can accumulate and be covered at the same time.

- Adaptable: You can change your investments by switching sub-funds when your financial needs change. In addition, you may also top up your investments and make partial withdrawals.

- Temporary pause of premium payments: If there is sufficient investment value in your policy, you can choose to pause premium payments to free up your cash flow without affecting your coverage.

Potential snags

- Penalties for early redemption: You may be penalised if you choose to terminate your insurance plan before a certain milestone is reached. Please refer to your insurance policy documents for more details.

- Rising insurance costs: Insurance charges rise with age. More fund units will be deducted to finance the insurance charges, resulting in a drag on investment returns.

- Investments and insurance are interlinked: Cashing investment returns out of your policy may reduce or even terminate your insurance coverage.

While there are many routes and modes of transport to get to your destination, the first step is having a plan. Knowing their respective benefits and potential snags, you can and should use a combination of the above investment instruments in your plan.

The following are some suggestions for your journey.

For new investors starting small

- Consider a portfolio of unit trusts and/or ETFs for lump-sum investments – this allows you to invest in a diversified portfolio with a low initial outlay. OCBC RoboInvest provides the additional convenience of smart portfolio rebalancing so you can stay on top of market opportunities.

Robo-advisors can be a part of your portfolio

- Robo-advisors are digital platforms that utilise automated solutions and algorithms to help you invest and manage your money. They offer a disciplined approach to investing that runs on autopilot.

- Timing of investments and portfolio rebalancing are done in specific intervals and runs on autopilot, removing human biases in the process.

- Of course, the algorithms and the investment methodology are produced by humans and may be tweaked from time to time. The ingredients for portfolio construction are typically ETFs, ensuring that investors are not taking concentrated exposure in any specific security.

- Robo-advisors tend to be low cost, passively managed, diversified and convenient. They offer rules-based type investment process that is relevant to individuals who would benefit from a strictly hands-off approach due to salience of behavioural biases in their investment decisions.

- Use regular savings plans (RSPs) to inculcate dollar cost averaging (Figure 3) into your investing discipline by investing monthly into unit trusts, ETFs and even blue-chip stocks via the OCBC Blue Chip Investment Plan.

You don’t really need much to start investing

Smaller board lots

Since beginning 2015, the Singapore Exchange (SGX) has decreased the standard board lot size for equities investment from 1,000 units to 100 units. This meaningfully decreases the amount of capital investors would need to buy stocks, making investments more accessible from a practical standpoint. It's easier to gain access to blue chips and index component stocks that tend to be higher-priced.

Growing retail bond market

The MAS has also introduced frameworks to make it easier for corporations to offer bonds to retail investors. Typically, purchase of a single corporate bond would set you back a heavy $200,000 to $250,000. Retail bonds are far more accessible with a $1,000 minimum investment.

Regular investment programmes

Regular investment programmes offered by banks help investors buy stocks and/or unit trust in a piecemeal fashion, exposing investors gradually to the stock market. It is another cost-effective investment solution that is akin to a strict monthly saving plan – the difference is that you save in stocks.

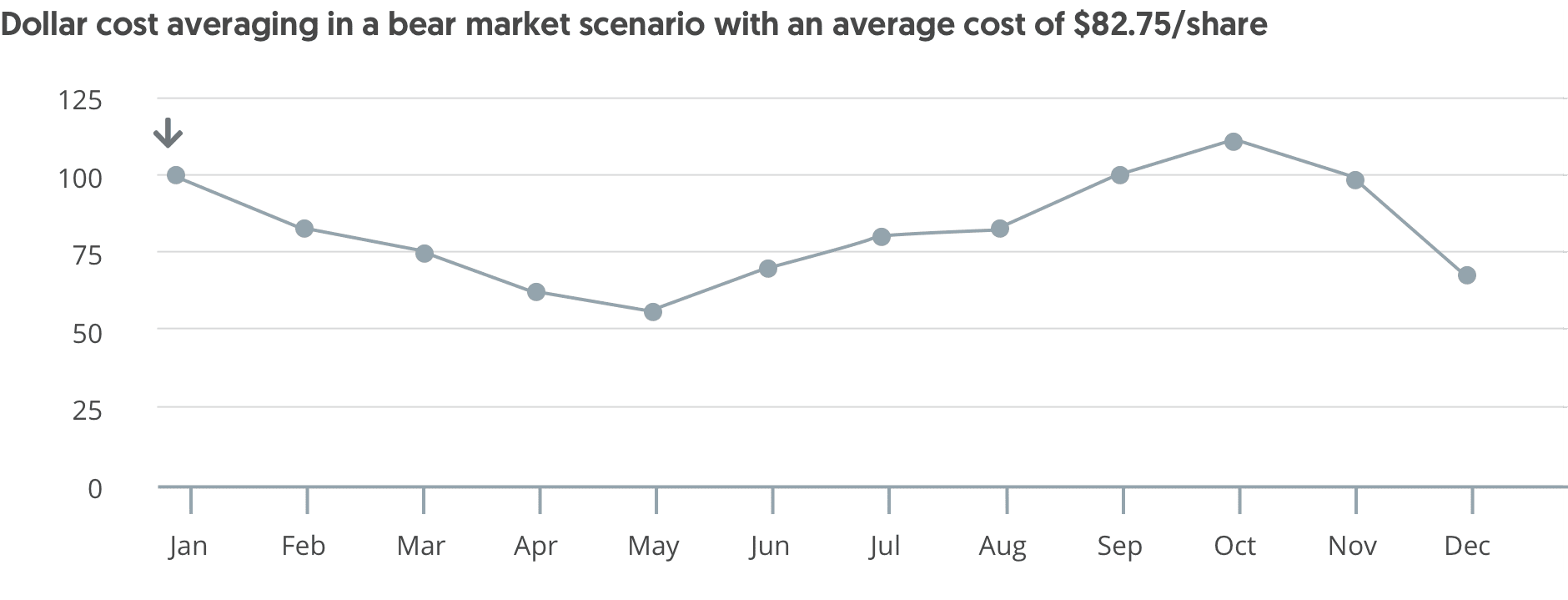

Figure 3: Difference between lump-sum investing and dollar cost averaging

Lump-sum investing in a bear market scenario with a cost of $100/share

Example: $12K investment

You invested $12,000 all at once in a single stock priced at $100/share in January. By the end of the year in December, a dip in the market hits and the stock fell to $70/share. You lose an immediate 30% of your investment (down: $3,600).

Example: $12K investment

You adopted a DCA strategy and invested $1,000 a month over a period of 12 months. Your average cost per stock is $82.75/share. You lose only ~15% of your investment (down: $1,848) despite the same drop in stock price from $100/share to $70/share.Source: OCBC Wealth Management

- Alternatively, if you prefer the convenience of a hybrid product that allows you to invest and insure yourself at the same time, consider an investment-linked life insurance plan (ILP).

For seasoned investors:

- Consider maintaining a diversified portfolio of unit trusts and/or ETFs as your core investment plan while carving out a smaller portion to invest tactically in direct equities and/or fixed income, or through structured investments.

- The core portfolio provides a greater level of stability and long-term returns while the tactical portfolio allows you to capture market opportunities.

- As your portfolio grows, consider adding more asset classes, such as gold and silver, dual currency investments and property (direct or REITs) for added diversification. This can help to further reduce overall portfolio volatility to the various market events.

Investing principles to live by

- Know your risk appetite and tolerance. Do not take on more risk than you are comfortable with, even if you are tempted by the potential of higher returns.

- Understand what you are investing in. This includes where returns may come from and the risks you need to be aware of.

- Diversify your portfolio across asset classes, regions, countries and sectors. This helps to reduce overall portfolio risks and make your journey less bumpy.

- Review your investment portfolio holistically together with your financial goals at least once a year. Changes to your family, job or health may require adjustments to your financial goals and thus affect your investment portfolio. OCBC Life Goals can help you to keep track of your progress.

- Keep yourself informed of market developments and seek professional advice where required.

Get started

OCBC: Your Trusted Partner in Wealth Management

Choosing the right bank is an important decision. You need a financial partner that is trustworthy, secure, and dependable. As a well-established bank in Singapore, OCBC has a long-standing reputation for financial strength. We are strictly regulated, committed to security, and dedicated to helping customers build their wealth with confidence. Whether you prefer traditional banking or digital investment solutions, OCBC provides a seamless and secure experience tailored to your needs.

Reliability: A Bank You Can Count On

With nearly a century of history, OCBC has demonstrated stability through economic shifts. OCBC is regulated by the Monetary Authority of Singapore. We also adhere to strict industry standards to ensure your investments are handled with integrity. Whether you're growing your wealth through traditional financial products or exploring digital investment options, you can rely on OCBC’s expertise and proven track record.

Recognized for Excellence

OCBC combines trust, security, and reliability to help you achieve your financial goals. Our digital wealth solutions make investing accessible and seamless, backed by expert guidance and strong security. We are honoured to be recognised as the Best Strongest Bank in Singapore by The Asian Banker 2024, a reflection of our commitment to excellence. If you’re looking for a bank that prioritizes your financial success, start your investment journey with OCBC today.

1Assuming this person is planning for S$2,900 in monthly expenses at the point of retirement with an estimated S$1,400 monthly payout from CPF LIFE from age 65 onwards.

General disclaimer

This advertisement has not been reviewed by the Monetary Authority of Singapore.

- Any opinions or views of third parties expressed in this document are those of the third parties identified, and do not represent views of Oversea-Chinese Banking Corporation Limited (“OCBC Bank”, “us”, “we” or “our”).

- This information is intended for general circulation and / or discussion purposes only. It does not consider the specific investment objectives, financial situation or needs of any particular person.

- Before you make an investment, please seek advice from your Relationship Manager regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs.

- If you choose not to do so, you should consider if the investment product is suitable for you, and conduct your own assessments and due diligence on the investment product.

- We are not making an offer, solicit to buy or sell or subscribe for any security or financial instrument, enter into any transaction or participate in any trading or investment strategy with you through this document. Nothing in this document shall be deemed as an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy.

- No representation or warranty whatsoever in respect of any information provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice.

- OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

- Investments are subject to investment risks, including the possible loss of the principal amount invested. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance.

- Any reference to a company, financial product or asset class is used for illustrative purposes and does not represent our recommendation in any way.

- The information in and contents of this document may not be reproduced or disseminated in whole or in part without the Bank’s written consent.

- OCBC Bank, its related companies, and their respective directors and/or employees (collectively “Related Persons”) may, or might have in the future, interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. OCBC Bank and its Related Persons may also be related to, and receive fees from, providers of such investment products.

- You must read the Offer Document/Indicative Term Sheet/Product Highlight Sheet before deciding whether or not to purchase the investment product, copies of which may be obtained from your relationship manager.

- Any hyperlink to any third party article, or other website or webpage (including any websites or webpages owned, operated and maintained by third parties) is for informational purposes only and for your convenience only and is not an endorsement or verification of any such article, website or webpage by OCBC Bank and should only be accessed at your own risk. OCBC Bank does not review the contents of any such articles, website or webpage, and shall not be liable to any person for the same.

Graphs, charts, formulae and other devices

Investors should note that there are necessarily limitations and difficulties in using any graph, chart, formula or other device to determine whether or not, or if so, when to, make an investment.

Global Equities Disclaimer

- Dividend growth is not guaranteed, nor are companies in which you invest obliged to pay dividends;

- Companies may go bankrupt rendering the original investment valueless;

- Equity markets may decline in value;

- Corporate earnings and financial markets may be volatile;

- If there is no recognised market for equities, then these may be difficult to sell and accurate information about their value may be hard to obtain;

- Smaller company investments may be difficult to sell if there is little liquidity in the market for such equities and there may be substantial differences between the buying price and the selling price;

- Equities on overseas markets may involve different risks to equities issued in Singapore;

- With regards to investments in overseas companies, foreign exchange rates may move in an unfavourable direction affecting adversely the valuation of investments in base currency terms.

Collective Investment Schemes

- A copy of the prospectus of each fund is available and may be obtained from the fund manager or any of its approved distributors. Potential investors should read the prospectus for details on the relevant fund before deciding whether to subscribe for, or purchase units in the fund.

- The value of the units in the funds and the income accruing to the units, if any, may fall or rise. Please refer to the prospectus of the relevant fund for the name of the fund manager and the investment objectives of the fund.

- Investment involves risks. Past performance figures do not reflect future performance.

- Any reference to a company, financial product or asset class is used for illustrative purposes and does not represent our recommendation in any way.

- The indicative distribution rate may not be achieved and is not an indication, forecast, or projection of the future performance of the Fund.

For funds that are listed on an approved exchange, investors cannot redeem their units of those funds with the manager, or may only redeem units with the manager under certain specified conditions. The listing of the units of those funds on any approved exchange does not guarantee a liquid market for the units.

Dual Currency Returns

- By buying Dual Currency Returns, you are giving us the right to repay you at a future date in a different currency from the currency in which you made your original investment, even if you would prefer not to be paid in this currency at that time. Dual Currency Returns are affected by foreign exchange rates, which may affect how much you get back from your investment. You may receive less than you originally invested.

- Foreign exchange control restrictions may apply to the foreign currencies linked to your Dual Currency Returns. As a result, we may repay your investment and interest in a different currency. You may receive less than you originally invested when the amount of this different currency is converted back to the base currency (the currency you originally invested). You may be able to get information on foreign exchange control restrictions, if any, for each foreign currency offered in relation to Dual Currency Returns, from the relevant monetary, regulatory or other governmental authorities for that currency.

- We will not end Dual Currency Returns before the maturity date (the date they are due to end). You may, however, withdraw the amount you originally invested before the maturity date. If you do this, please remember that you will have to pay any charges that apply which are calculated based on the amount of the time remaining before maturity date, as well as current market conditions relating to strike prices, foreign exchange rates and changes in the underlying foreign exchange pair. These charges may mean that you get back much less than you originally invested. Please feel free to approach your relationship manager for details of the procedures and charges that apply if you withdraw your Dual Currency Returns investment before the maturity date.

- Dual Currency Returns are not insured deposits for the purposes of the Deposit Insurance and Policy Owners’ Protection Schemes Act of Singapore.

Policy Owners' Protection Scheme

This plan is protected under the Policy Owner's Protection Scheme which is administered by the Singapore Deposit Insurance Corporation (SDIC). Coverage for your policy is automatic and no further action is required from you. For more information on the types of benefits that are covered under the scheme as well as the limits of coverage, where applicable, please contact us or visit the Life Insurance Association (LIA) or SDIC websites (www.lia.org.sg or www.sdic.org.sg).

Important notice for Insurance

The insurance plans are provided by The Great Eastern Life Assurance Company Limited, a wholly-owned subsidiary of Great Eastern Holdings Limited and a member of the OCBC Group and Transamerica Life Bermuda Ltd. The insurance plans are not bank deposits and OCBC Bank does not guarantee or have any obligations in connection with it.

You may want to seek advice from a financial adviser before committing to buy the product. If you choose to not seek advice from a financial adviser, you should consider if the product is suitable for you.

Buying a life insurance policy is a long-term commitment. An early termination of the policy usually involves high cost and the surrender value payable may be less than the total premiums paid.

This document is for general information only. It is not a contract of insurance or an offer to buy an insurance product or service. It is also not meant to provide any insurance or financial advice. The specific terms and conditions of the plan are set out in the policy documents. If you are interested in the insurance policy, you should read the product summary and benefit illustration (available from us) before deciding whether to buy this product. We do not guarantee, represent or warrant that any of the information provided in this document is accurate and you should not rely on it as such. We do not undertake to update the information or to correct any inaccuracies. All information may change without notice. We will not be liable for any loss or damage arising directly or indirectly in connection with or as a result of you acting on the information in this document. This document may be translated into the Chinese language. If there is any difference between the English and Chinese versions, the English version will prevail.

Foreign Currency Disclaimers

- Foreign currency deposits are subject to inherent exchange rate fluctuation that may provide opportunities and risks. Consequently, exchange rate fluctuations may affect the value of your foreign currency investments or deposits.

- Earning on foreign currency investments or deposits may change depending on the exchange rates prevalent at the time of their maturity if you choose to convert.

- Exchange controls may apply to certain foreign currencies from time to time.

- Any pre-termination costs will be taken and deducted from your deposit directly and without notice.

- Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.