Export Documentary Collection 101 – Improve your working capital

Export Documentary Collection 101 – Improve your working capital

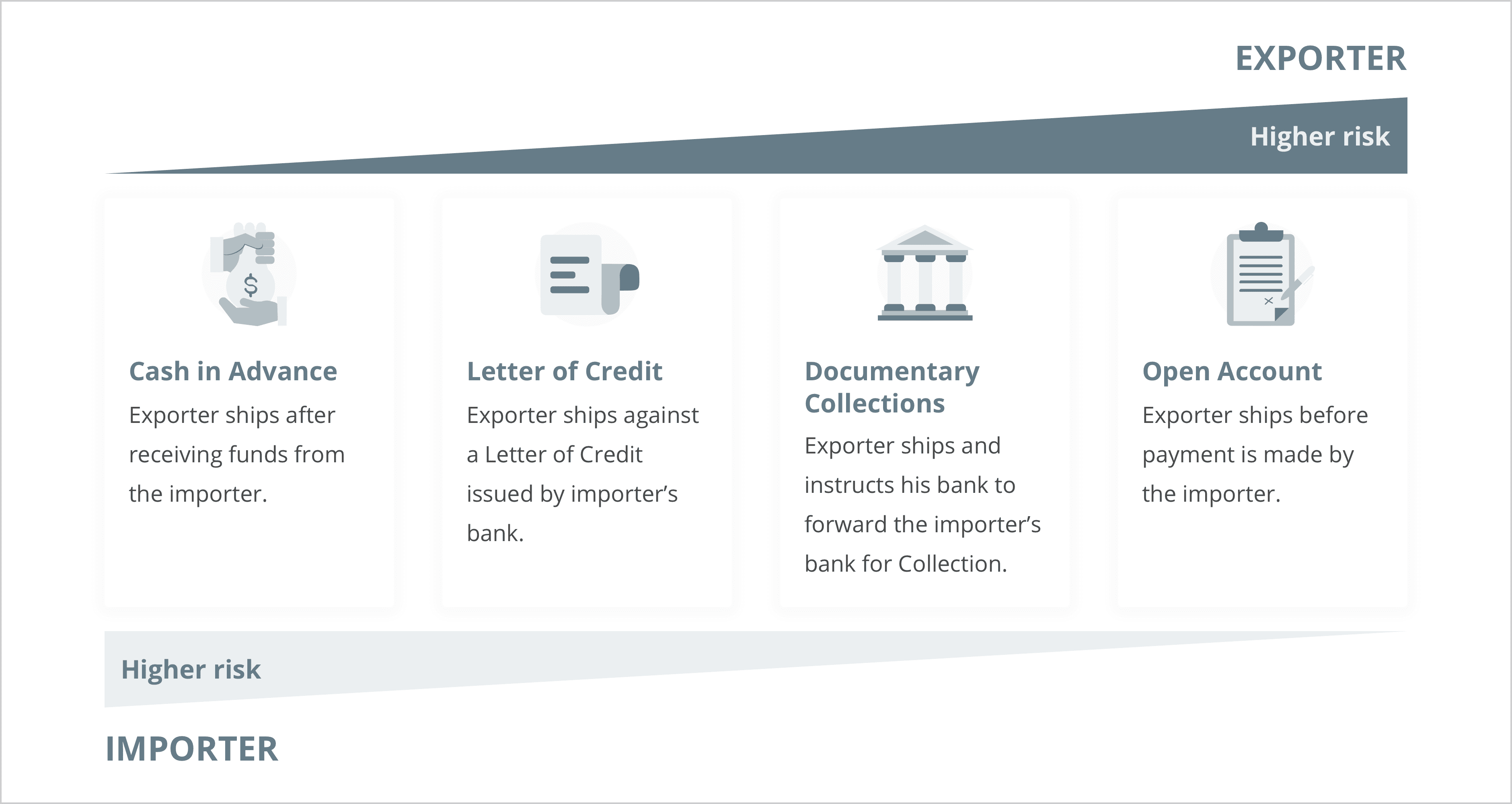

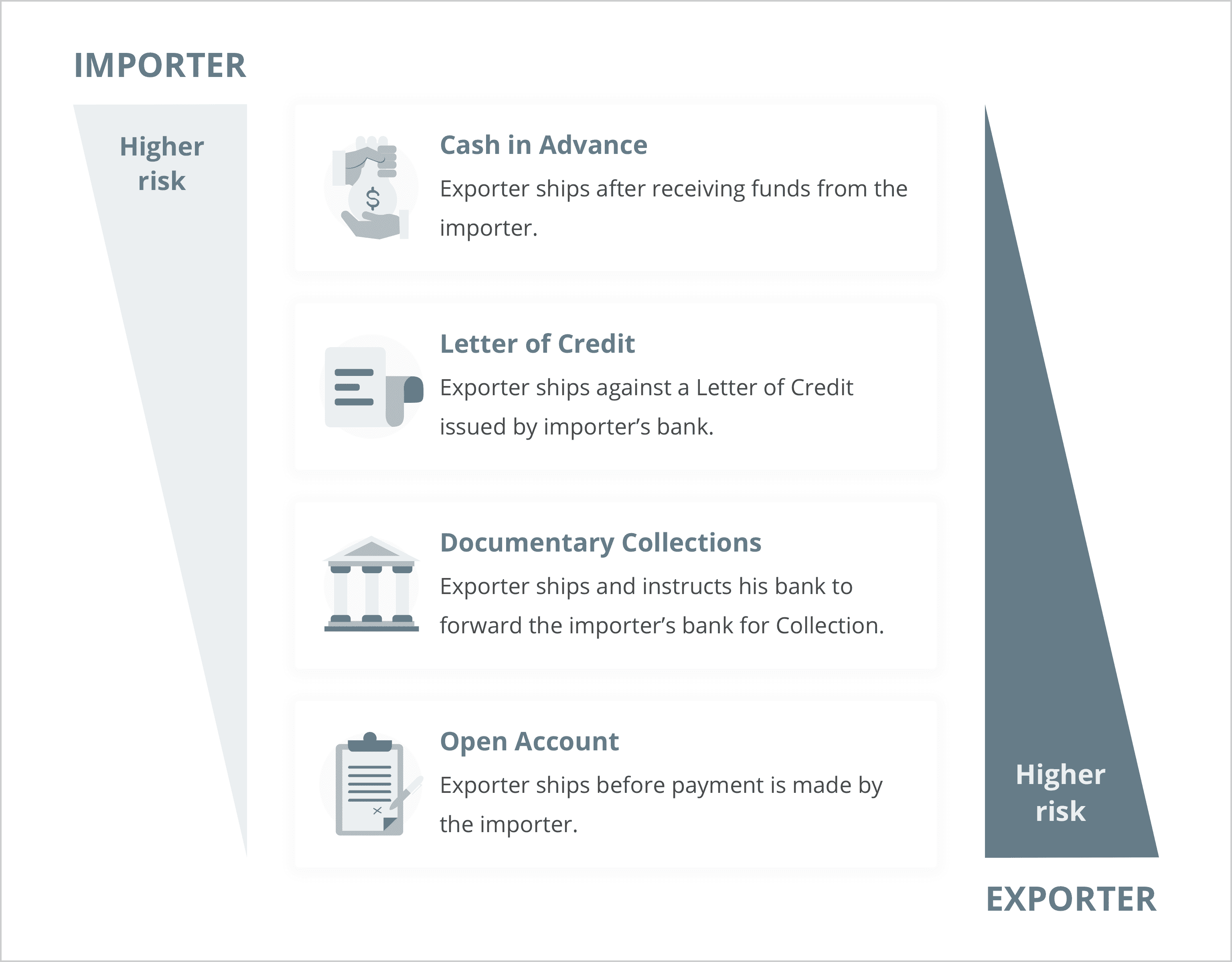

Selling goods internationally always entails some degree of risk for both the exporter and the importer. Therefore, there is also a balance that must be struck. Full risk protection for the exporter (i.e. through cash-in-advance terms) means the importer is bearing all the risk. The reverse is also true. Open account terms mean full risk protection for the importer and complete risk-bearing by the exporter.

The good news is that there are several trade financing instruments that allow both parties to meet in the middle. In our previous article, we looked at Letters of Credit (LC), whereby the exporter can trust the importer’s bank to fulfil the LC obligations. In this article, we are going to explore the core details of another popular instrument – Export Documentary Collection.

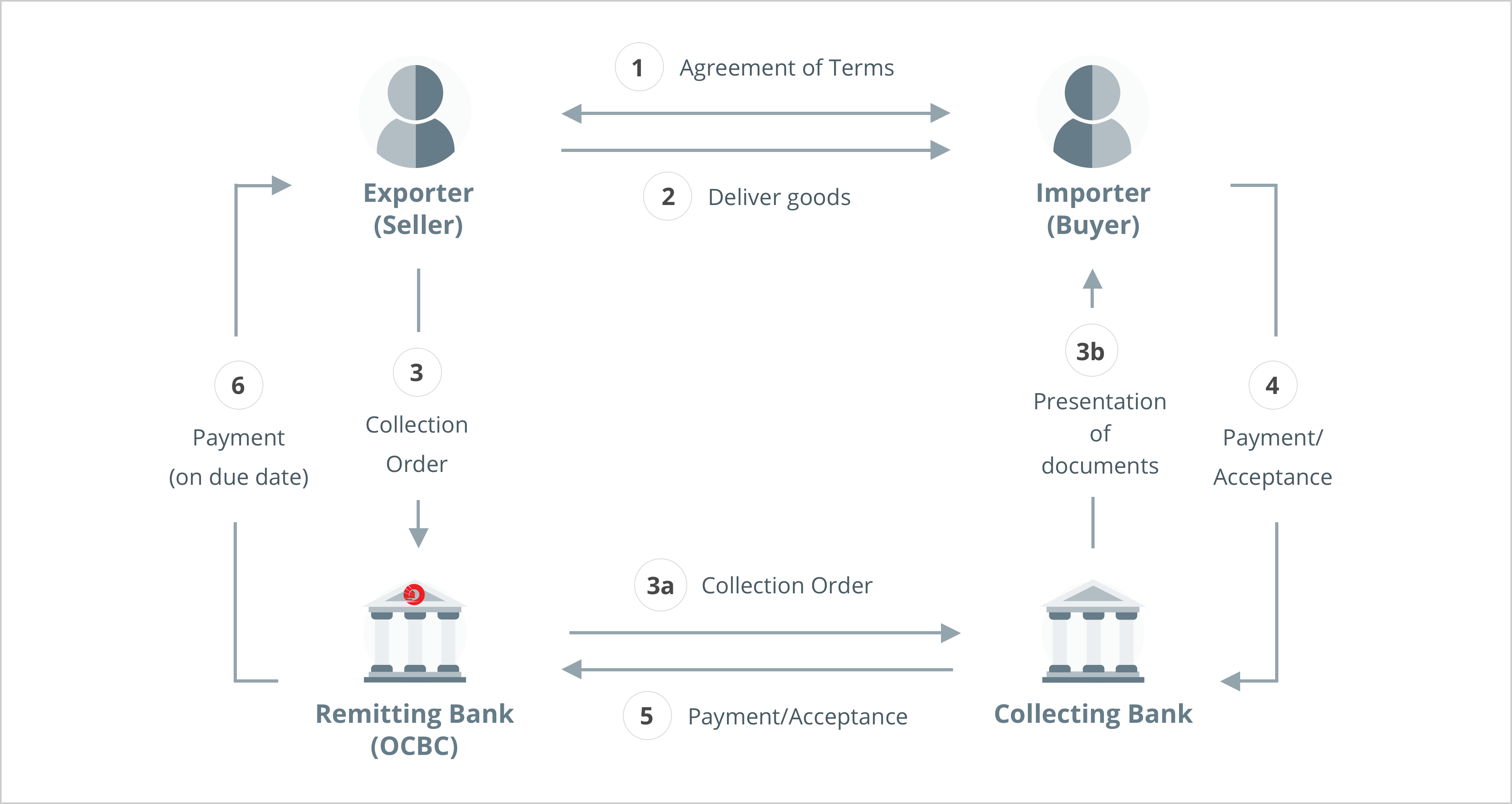

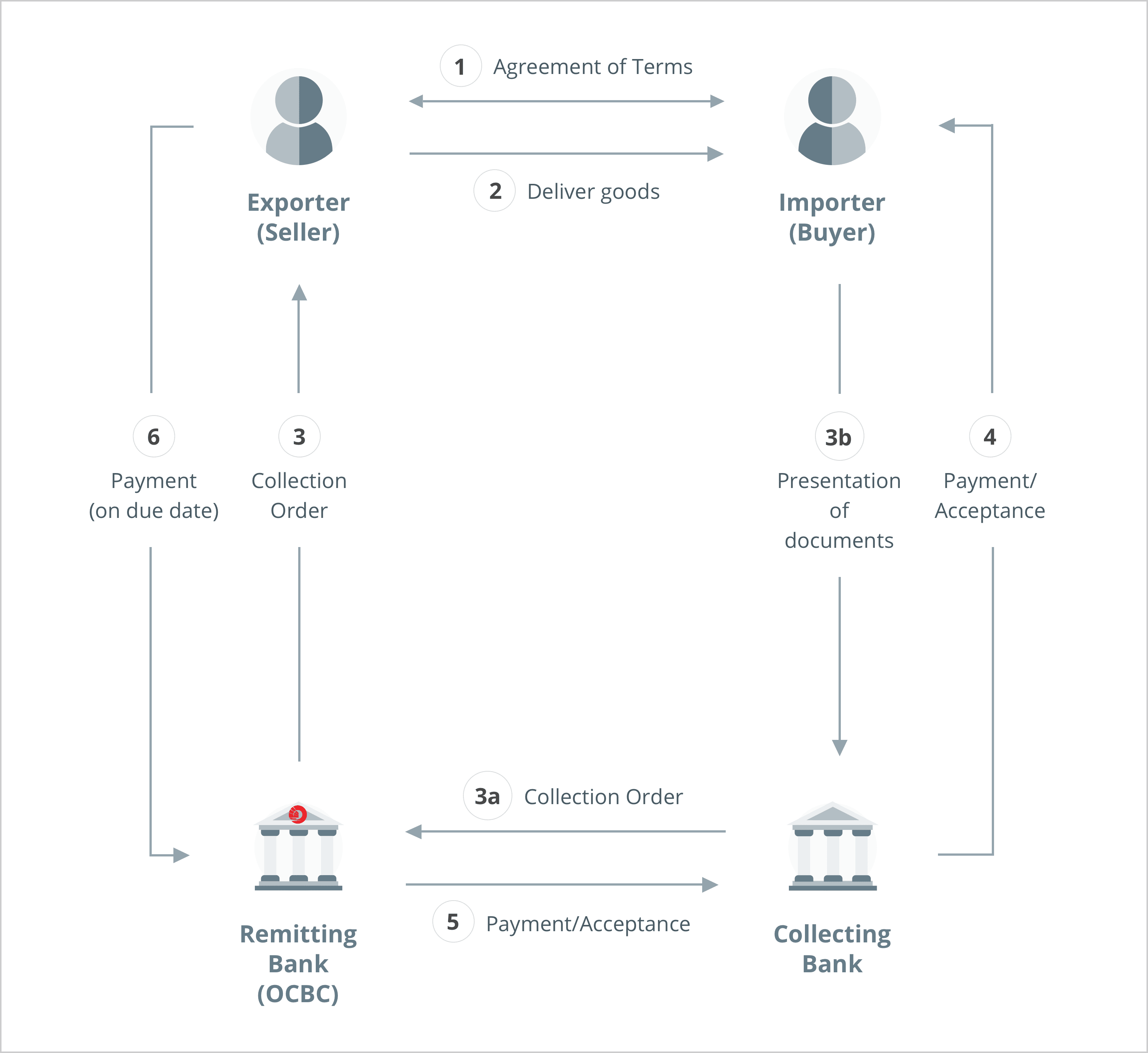

Export Documentary Collection involves the importer paying the exporter upon receiving the required documents. The banks – for both the importer and exporter – function as intermediaries to facilitate the transaction. Let's get a better understanding of how this whole process works.

A step-by-step guide to understanding Export Documentary Collection

Broadly speaking, from your perspective (as the exporter), the Export Documentary Collection process can be broken down into five steps:

1. Agreement of terms:

You and your importer agree to the transaction and payment terms, including the use of Export Documentary Collection. At this point, you should also negotiate whether it will be:

- Documents against acceptance (DA) – where documents relating to the sale of goods will be availed once the importer has given his acceptance to make the payment at a later date.

- Documents against payment (DP) – where documents will be availed to the importer once the payment has been made and finalised.

2. Shipment and receipt of documents:

You ship the goods and receive documents from the carrier or freight forwarder, proving that the shipment has occurred.

3. Presentation of documents to the bank:

First, complete the Export Documentary Collection application form and the bill of exchange draft. Next, present these documents together with your shipping documents to OCBC, which is also known as the remitting bank in this process. Your remitting bank will then proceed to:

- Forward these documents to your importer’s bank, known as the collecting bank.

- The collecting bank will then inform your importer that the documents have arrived and release the documents once payment conditions have been met (this depends on whether your payment term is DA or DP as explained in step 1 above).

4. Receipt of payment from the importer and possession of goods:

The importer will make payment to its bank via DA or DP (as explained above) and take possession of the documents.

5. Receipt of payment from OCBC to the exporter:

OCBC will then credit into your account upon receiving the receipt of the funds from the importer’s bank, either immediately (when the situation involves DP) or at the predetermined date of the accepted bill of exchange (when the situation involves DA).

Key benefits of Export Documentary Collection for exporters

First, the control factor. Although, as explained, there is still risk involved, Export Documentary Collection allows you to retain control of the goods until they are paid for or acceptance from the importer is received. Here, having a trusted and reliable bank as your intermediary to handle your documents will help.

Next, some banks like OCBC also offer Export Bill Purchase if you need to shorten your working capital cycle even further (subject to credit assessment). This is a form of short-term financing where you can obtain cash in advance based on the export documents. This is also particularly helpful for DA terms.

Risks associated with Export Documentary Collection

To explain the level of protection that Export Documentary Collections provide to the exporters, we compare it with Letter of Credit (LC). In a LC, there is assurance to the exporter that its bank will fulfil its obligations. As long as the LC terms and conditions are complied with, the primary risk for the exporter is the risk of the importer’s bank and country.

In the case of Export Documentary Collection however, there is no transfer of risk. Here, the banks function solely as agents for remitting documents and payments. The degree of risk borne by the exporter depends on whether the transaction is conducted on DA or DP terms.

When DA applies, exporters are completely exposed to the risk of non-payment or default from the importer. Of course, the acceptance from the exporter can be used as a basis for pursuing legal action, but that itself carries its own costs.

DP provides slightly greater comfort for exporters, since the importer must make the payment before they are able to collect the documents.

In a nutshell, Export Documentary Collection exposes both the exporter and importer to risks. DP leans more toward the exporter while DA leans more toward the importer. There is no recourse to any third party, meaning this financing instrument should only be used in:

- Higher-trust situations where both parties know each other fairly well; and

- Countries with strong legal systems and contract enforcement.

That said, if both the criteria are met, then Export Documentary Collection can offer clear benefits to exporters.

Let OCBC be your trusted banking partner in your international business journey

OCBC has helped thousands of businesses in their international business journey by providing them valuable trade financing services. We can help with yours too, whether you are using our Export Documentary Collection or Export Letter of Credit services. We also have a full suite of SME Trade Financing Solutions that even domestic-focused businesses can benefit from as well.

You may be directed to third party websites. OCBC Bank shall not be liable for any loss suffered or incurred by any party for accessing such third party websites or in relation to any product and/or service provided by any provider under such third party websites..

Discover other articles about: