Three key sustainability trends for 2026

Three key sustainability trends for 2026

Summary

Despite headwinds from heightened geopolitical tensions and economic uncertainty, the green economy has shown resilience with sustained investment growth in key sectors.

This report highlights three key sustainability trends to watch in 2026:

- the resilience of the global energy transition,

- the need to scale decarbonisation levers in the face of increasing sustainability -related costs, and

- the emerging sustainability -related challenges and opportunities amid the AI boom.

1. Staying the course on the global energy transition

The global energy transition demonstrated resilience in 2025 despite geopolitical headwinds and trade tensions, with this trend expected to continue in 2026. Although geopolitics and shifts in US climate policy are creating uncertainty in the market, the global drivers for clean energy remain robust, including increasing affordability and countries recognising the importance of diversifying energy sources.

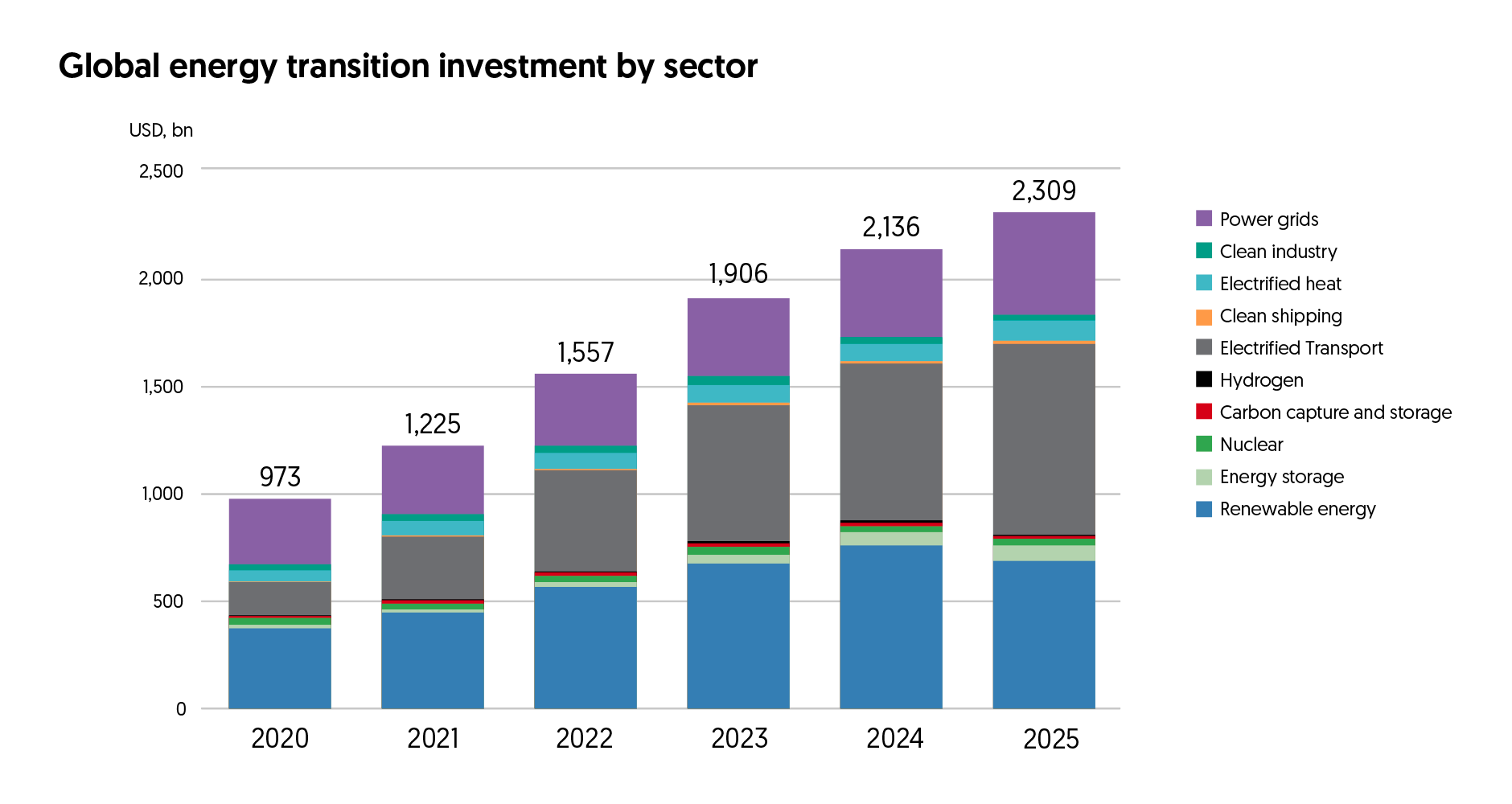

Global energy transition investment reached an all -time high of USD2.3trn in 2025, up 8% from the previous year, according to BloombergNEF. Electrified transport represented the largest sector of energy transition investment in 2025, with USD893bn invested in the purchase of electric vehicles (EVs) and the development of charging infrastructure. Renewable energy, the second largest sector in global energy transition investment, secured USD690bn in new investment, led by solar.

Source: BloombergNEF, OCBC Group Research

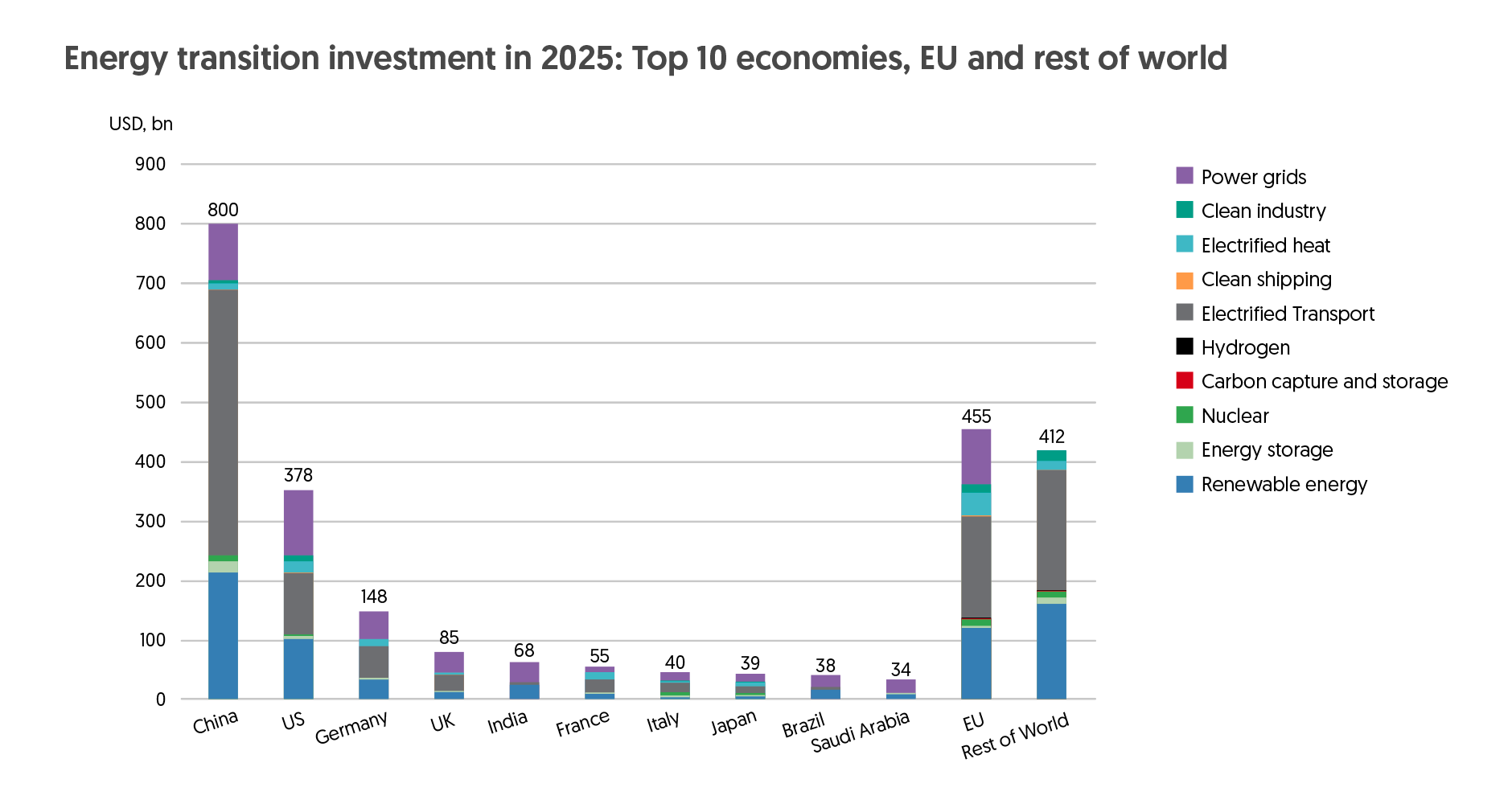

Despite a 3.8% year-on-year decline in China’s energy transition investment to USD800bn in 2025 driven by power market reforms, China still retains its position as the largest market for energy transition investment. Although China’s total electricity consumption in 2025 reached a record high of 10.4trn kWh, the country’s thermal power generation fell for the first time in 10 years by 1%. Clean energy growth in China met the growth in electricity demand, and the upward trend in clean energy generation is expected to continue in 2026.

Source: BloombergNEF, OCBC Group Research

China’s continued strong momentum in clean energy expansion, including nuclear energy, is progressing in parallel with efforts to address rising renewable energy curtailment. China aims to establish a new grid system to support a west-to-east power transmission exceeding 420GW by 2030, according to a guidance issued by the National Energy Administration and the National Development and Reform Commission. It has also commissioned four new ultra-high voltage transmission lines in 2025, raising cross-provincial transmission capacity to 370GW, in addition to accelerating the construction of energy storage facilities. Continued investment in grid infrastructure and transmission capacity is key to reducing rising renewable energy curtailment rates in China, although the rapid expansion of renewables currently continues to outpace grid upgrades.

In the EU, energy transition investment grew by 18% year-on-year to USD455bn and contributed the most to the global increase in 2025. Wind and solar power generated more electricity than fossil fuels for the first time last year. Renewables and nuclear power combined accounted for 71% of EU’s electricity mix in 2025, with solar now providing more than one-fifth of electricity in countries such as Hungary, Spain and the Netherlands. This highlights the EU’s ongoing shift towards low-carbon energy despite geopolitical headwinds.

2. Scaling decarbonisation levers amid rising sustainability costs

Companies worldwide are navigating an uncertain landscape of sustainability-related reporting and regulations, with compliance costs expected to rise in the coming years. Some drivers and implications of rising compliance costs are elaborated in the table below.

These sustainability-related reporting and regulatory developments are expected to drive greater investment in decarbonisation levers, especially for hard-to-abate sectors that are incentivised to reduce emissions and their associated rising costs.

| Drivers | Examples | Implications |

|---|---|---|

| Carbon pricing mechanisms | 80% increase in Singapore’s carbon tax, plans to implement carbon tax in Malaysia and Indonesia, China ETS expansion | Emissions -intensive sectors face rising carbon prices, which incentivise investment in low -carbon solutions and carbon credits, while encouraging the reduction of stranded asset risk associated with coal assets |

| EU trade regulations | EU’s Deforestation Regulation (EUDR) and Carbon Border Adjustment Mechanism (CBAM) | EU trade partners may pivot to alternative trade markets and reshape supply chains, although simplification efforts are ongoing to reduce trade partners’ administrative burden |

| Evolving sustainability-related reporting requirements | Mandatory ISSB-aligned reporting, EU’s Corporate Sustainability Reporting Directive (CSRD), EU’s Corporate Sustainability Due Diligence (CSDDD), China’s Corporate Sustainability Disclosure Standards (CSDS) | Mandatory reporting requirements on climate-related and nature-related risks and opportunities are increasing globally, highlighting the need to enhance reporting capabilities and address data limitations e.g. Scope 3 emissions |

| Global sector-specific market-based scheme | CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation) | Measures to decarbonise international aviation are being enhanced through innovative aircraft technologies, streamlining flight operations, deploying sustainable aviation fuel (SAF) and purchasing CORSIA-eligible carbon credits |

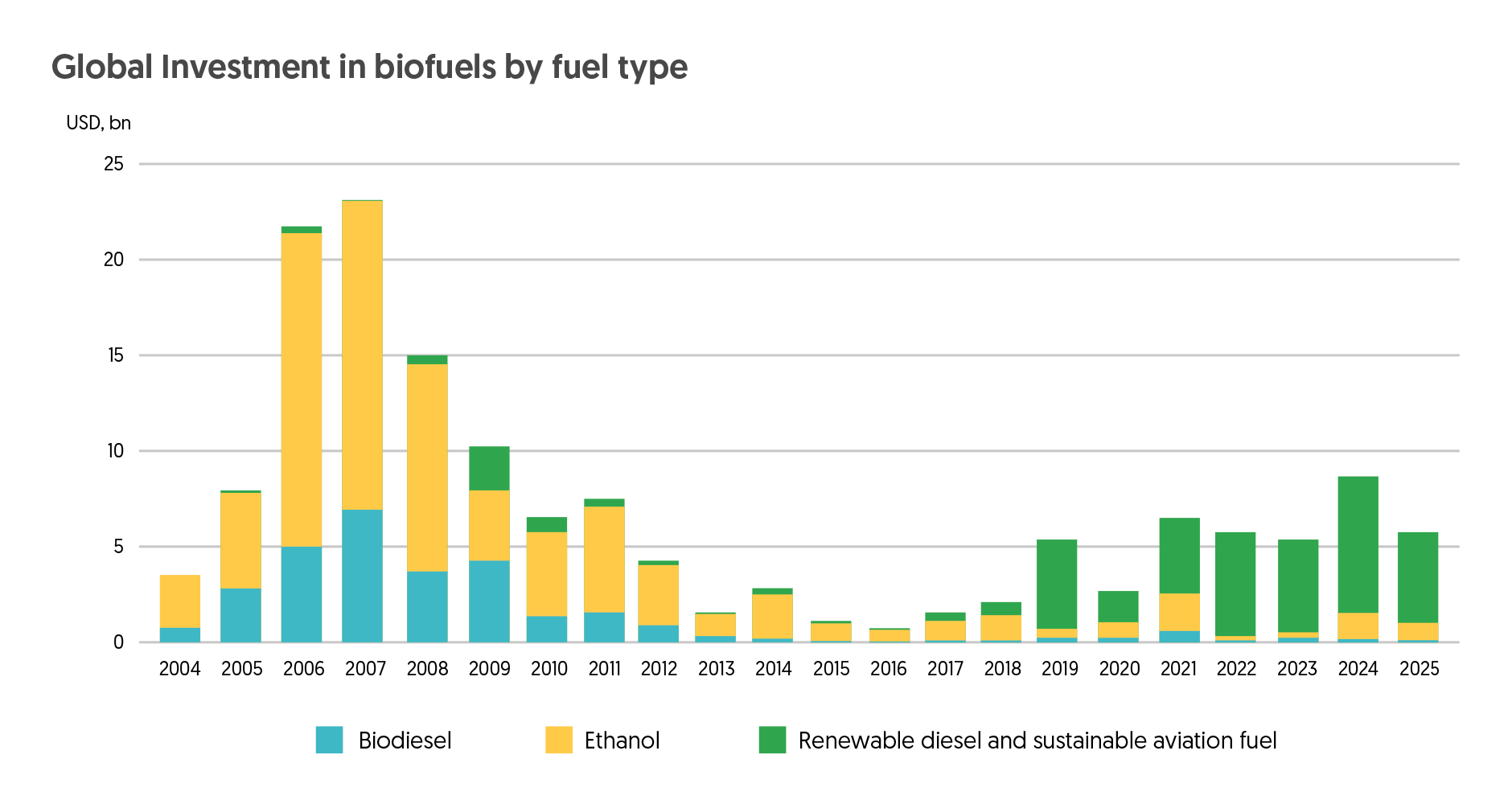

For example, the aviation sector is a hard-to-abate sector that is heavily dependent on fossil fuels and subject to reporting and offsetting requirements under CORSIA. SAF is a biofuel viewed as a critical decarbonisation lever for the aviation sector to achieve net-zero carbon emissions by 2050. Global biofuel investment remains focused on drop-in1 fuels like SAF and renewable diesel, which collectively comprised 86% of total global biofuel investment in 2025, according to BloombergNEF.

This trend is driven by aviation sector net-zero commitments, as well as SAF blending mandates, levies and incentives in several markets. SAF blending mandates went into effect in the EU and UK in 2025 i.e. SAF blending targets of 6% in the EU and 10% in the UK by 2030. Mandates will soon take effect in some APAC markets, such as Singapore (1% SAF blending target for 2026, targeting to rise to 3-5% by 2030), South Korea (1% SAF blending target by 2027, targeting to rise to 3-5% by 2030 and 7-10% by 2035) and Indonesia (1% SAF blending target by 2027, up to 5% in 2029). To support Indonesia’s SAF production capabilities, the country plans to ban the export of palm oil waste and direct it towards domestic biodiesel and SAF production. This can reduce Indonesia’s reliance on imported fuel, enhance energy security and contribute to the decarbonisation of the aviation sector

1Drop-in fuels are biofuels or synthetic fuels designated to be blended with conventional petroleum -derived hydrocarbons. They can therefore be used without major modifications of the engine or the fuel system.

Source: BloombergNEF, OCBC Group Research

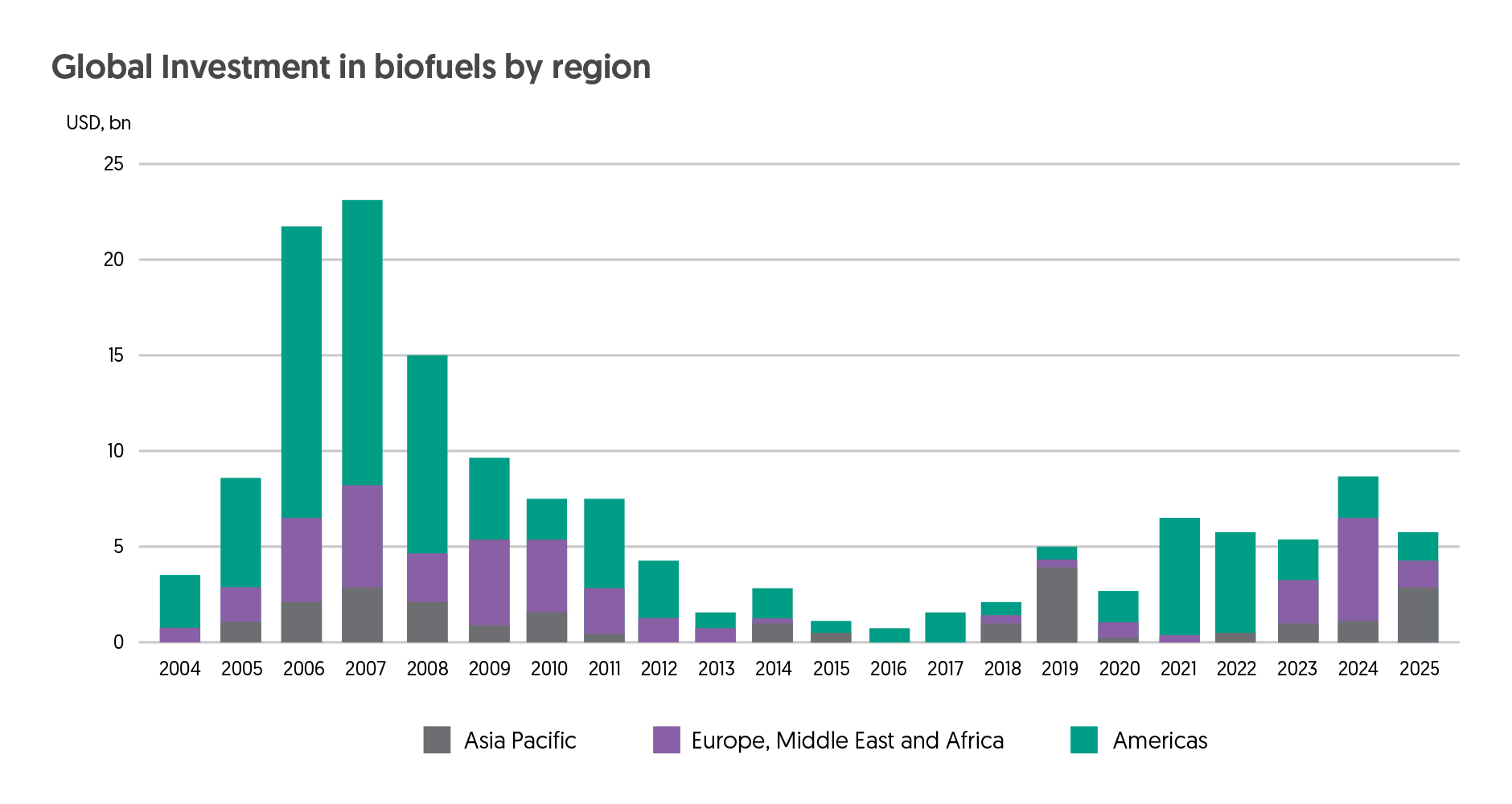

Although global biofuel investment fell by 27% year-on-year to USD6.2bn in 2025, investment in APAC doubled. This growth was primarily driven by China, which is leading SAF investment in APAC and globally, despite the absence of SAF blending mandates. With investment in the Americas led by the US, policy changes under the Trump administration have reduced SAF incentives, resulting in a 17% year-on-year decrease in biofuel investment in 2025. Meanwhile, the EU, Middle East and Africa experienced an increase in biofuel investment in 2023 – 2024 in anticipation of sustainable aviation policies taking effect. The 2025 decline could represent a recalibration period until policy support ramps up in the coming years.

Source: BloombergNEF, OCBC Group Research

To support the decarbonisation of residual emissions in hard-to-abate sectors and the achievement of countries’ climate targets, there has been an enhanced focus on scaling the supply of high-quality carbon credits as demand increases. Carbon credits are viewed as a complementary decarbonisation lever, including carbon credits aligned with Article 6 of the Paris Agreement, CORSIA-eligible carbon credits and transition credits.

Carbon market players are developing shared principles on the voluntary use of high-integrity carbon credits across jurisdictions, concurrently aiming to scale supply to meet rising demand. COP30 last year saw the formation of the Open Coalition on Compliance Carbon Markets and The Coalition to Grow Carbon Markets, aiming to improve the effectiveness of carbon pricing and strengthen the voluntary demand for carbon credits respectively.

There has also been progress in bilateral carbon credit agreements under Article 6.2 of the Paris Agreement, which enables countries to transfer carbon credits generated from the reduction of emissions to support each other in meeting their national climate targets. For example, Singapore and Rwanda recently launched an application call for carbon credits under their Implementation Agreement on carbon credits cooperation, which marks Singapore’s fourth call for project applications following earlier calls under similar agreements with Ghana, Peru and Bhutan. As carbon tax-liable companies can use eligible high-quality, Article 6-compliant international carbon credits to offset up to 5% of their taxable emissions, the demand for such carbon credits as a decarbonisation lever is expected to grow alongside Singapore’s rising carbon tax.

3. Emerging challenges and opportunities linked to the AI boom

The AI boom poses a dilemma as it can enable new and more efficient applications that could reduce emissions and other climate-related risks, yet its increasing resource demands may also exacerbate these risks.

The exponential growth of the data centre (DC) industry, driven by AI and cloud services demand, puts significant pressure on energy supply, grid capacity, emissions and water availability. AI systems, especially those powered by deep learning and large language models (LLMs), are highly energy-intensive and water-intensive. With the rapid expansion of AI-driven DCs, the industry’s power consumption is projected to nearly double between 2024 and 2030, with water use for cooling systems expected to follow a similar trend.

There are constraints in meeting the rising energy demand from DCs solely through clean energy sources. In response to the urgent need for capacity expansion, some companies are attempting to bring decommissioned nuclear power plants and gas/coal-fired power plants back online. However, this approach must be balanced against the risk of stranded assets amid the ongoing global transition away from fossil fuels. This trend is expected to favour energy producers that can bridge the emerging energy gap, particularly those with scalable clean energy generation capacity e.g. nuclear or renewable energy sources. In addition, transmission lines, grid interconnections and supporting grid infrastructure require significant capital investment to address grid limitations that are expected to come with exponential DC industry growth.

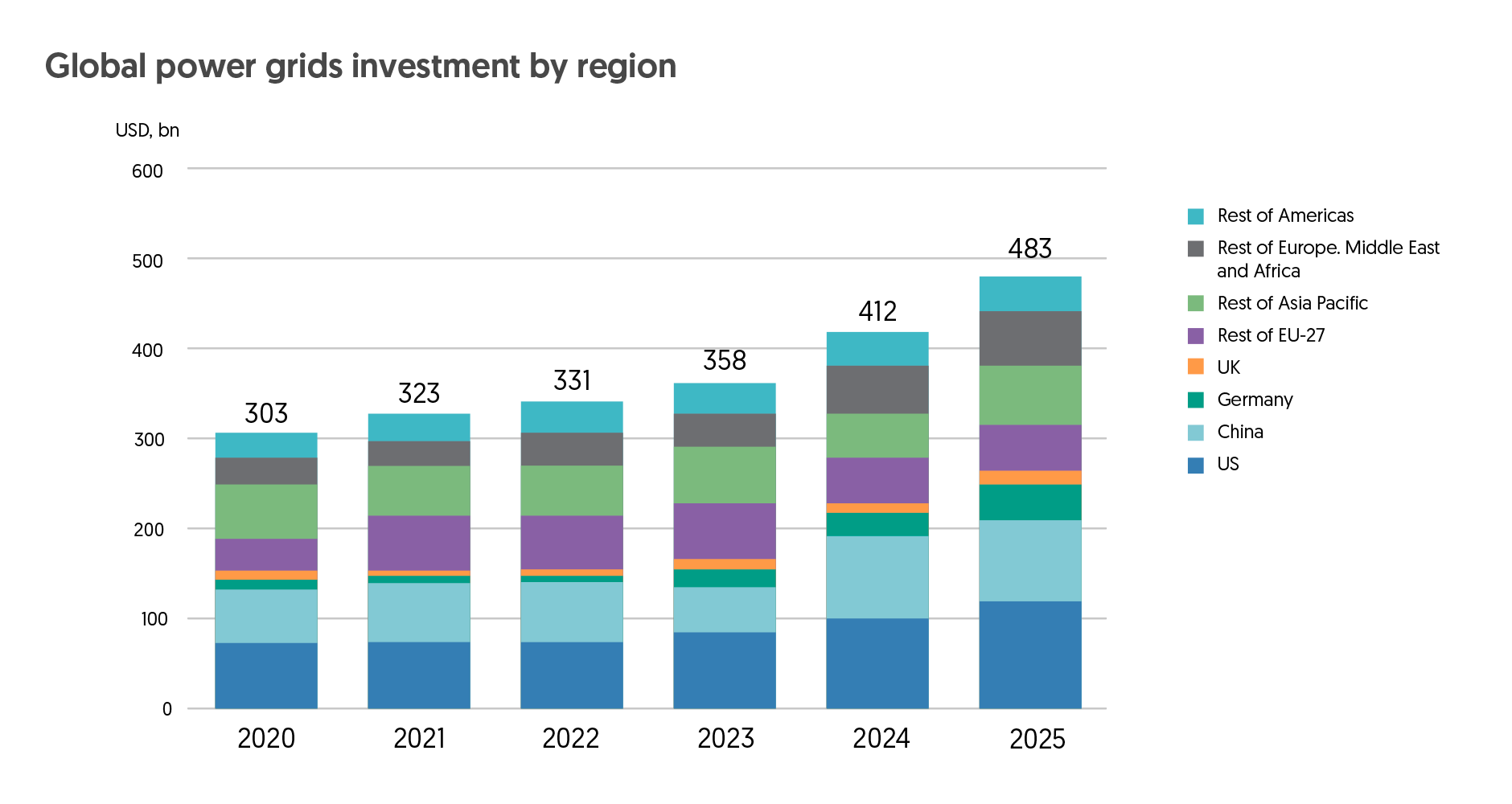

Global investment in power grids rose to a record USD483bn in 2025, representing a 17% year-on-year increase. The US and China accounted for the two largest shares of investment, at 24% and 20% respectively. The UK and Germany experienced the highest year-on-year investment growth, at 44% and 33% respectively, driven by large transmission projects aimed at linking offshore wind capacity with rapidly growing demand hubs. For example, Britain’s National Grid and Germany’s TenneT Germany will collaborate to develop a power link called GriffinLink, connecting British and German offshore wind farms in the North Sea to supply both countries. The interconnector could connect up to 2GW of offshore wind to both countries and is expected to be operational by the late 2030s.

Source: BloombergNEF Grid Investment Outlook 2025, OCBC Group Research

The acceleration of grid investment accompanies rising demand growth from AI-driven DCs and electrification. This trend puts pressure on both emerging and developed economies to enhance grid stability through initiatives such as incorporating energy storage systems and replacing aging assets.

For ASEAN, the increase in grid investment presents an opportunity to advance the ASEAN Power Grid (APG) vision by improving cross-border transmission capacity and system interoperability. Enhanced grids can facilitate cross-border low-carbon electricity trade between member states, balance regional demand fluctuations and strengthen regional energy security.

The use of AI also presents significant growth opportunities in numerous sustainability-related applications across diverse sectors. AI-driven tools can be implemented in areas such as climate modelling and planning, improving forest/crop monitoring and management, optimising operational efficiency of manufacturing facilities, as well as automating the monitoring, reporting and verification (MRV) of carbon sequestration projects.

With the AI boom, it is critical for economies to balance the complexities of accommodating rising AI-driven resource consumption, ensuring grid reliability, capturing growth opportunities, while preventing power costs from rising too rapidly.

Important information

This advertisement has not been reviewed by the Monetary Authority of Singapore. General Disclaimers Foreign Currency Global Equities Disclaimer Dual Currency Returns Collective Investment Schemes Cross Border Market Disclaimers