Embodied carbon: Revealing unseen emissions in the built environment

Embodied carbon: Revealing unseen emissions in the built environment

Summary

The built environment accounts for around 40% of global carbon emissions, with embodied carbon being especially critical with the rising demand for construction materials. The cement and steel sectors’ low-carbon transition can be accelerated through scaling low-carbon solutions, harmonising standards, prioritising embodied carbon reduction, as well as bridging the price gap between green and conventional construction materials.

What is embodied carbon?

Emissions in the built environment comprise two types:

- Operational carbon, associated with the energy used to operate the building (including fugitive refrigerant emissions), and

- Embodied carbon, associated with materials and construction processes over a building’s lifetime.

Nearly one third of all building-related emissions stem from embodied carbon, which accounts for around 10% of all energy-related greenhouse gas emissions worldwide, according to the World Green Building Council.

The proportion of embodied carbon in the built environment could increase to around 50% by 2035, as operational emissions of buildings decrease due to rising operational efficiency, according to the Global Real Estate Sustainability Benchmark (GRESB). Operational carbon has received more attention through policies and targets addressing buildings’ energy efficiency, whereas embodied carbon faces challenges such as a lack of reliable emissions data for building materials. Nonetheless, its importance in assessing the climate impact of the built environment is growing, as it has become a material issue for developers and investors.

Concrete and steel as major contributors to embodied carbon

Building elements such as foundations, frames and other forms of superstructure represent the largest proportion of embodied carbon in the built environment. These materials are used in large volumes and often contain emissions-intensive materials such as concrete and steel. These hard-to-abate construction materials are particularly difficult to decarbonise due to the nature of their production processes, where emissions result from both chemical reactions and the high temperature heat requirements that to date rely mainly on fossil fuels:

- Concrete is a composite material primarily made of coarse and fine aggregates, cement and water. Approximately 90% of total carbon emissions from concrete production comes from cement production due to its manufacturing process. The calcination process from heating limestone to produce clinker releases CO2, while fossil fuel combustion used to reach the high temperatures (~1,450°C) required in kilns contributes significantly to emissions.

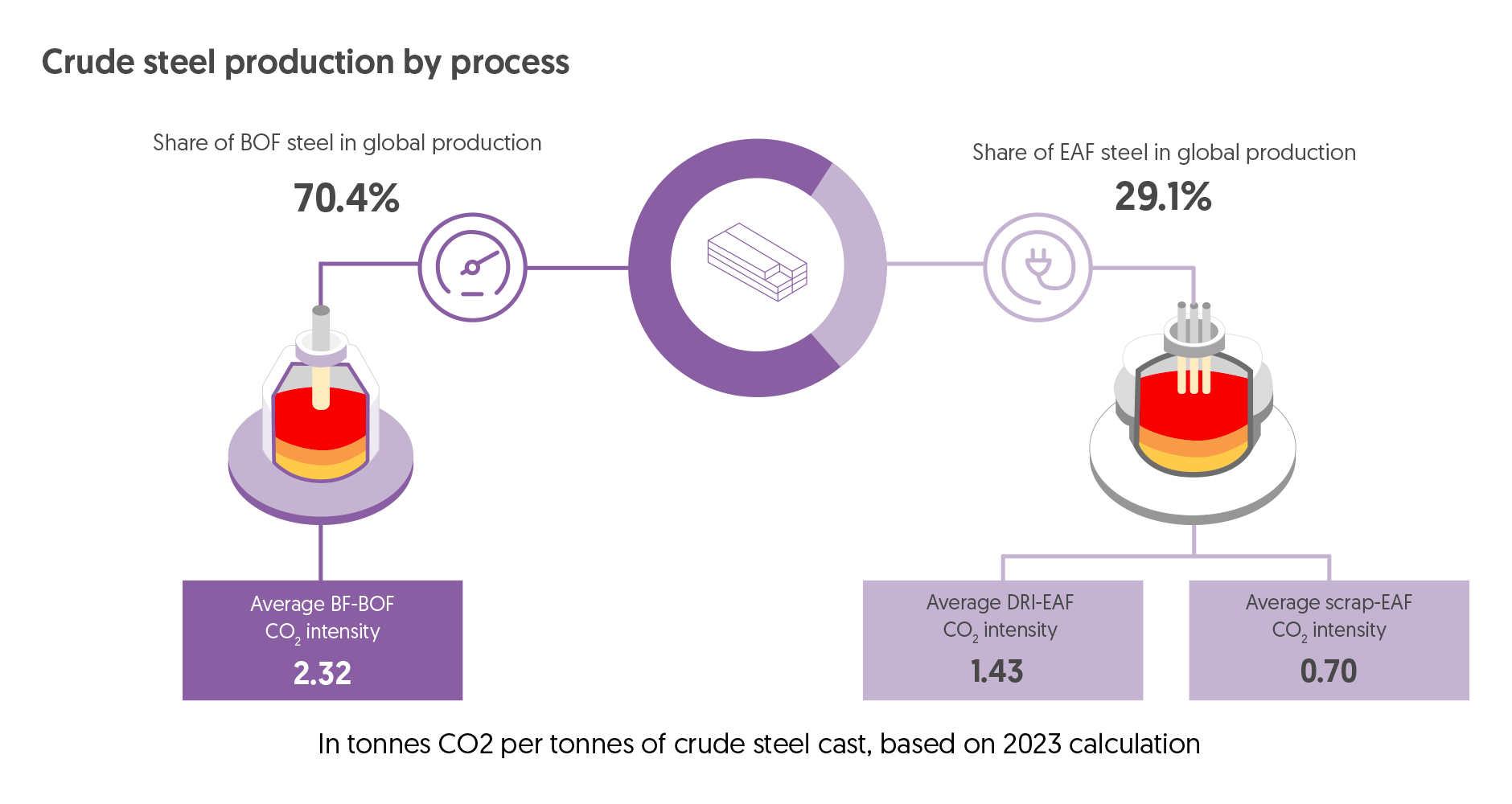

- The production of steel currently accounts for 7–8% of emissions globally. The prevailing steelmaking method, blast furnace–basic oxygen furnace (BF-BOF), relies heavily on coal used as a reducing agent to extract iron from iron ore. While BF-BOF accounts for around 70% of global steel production and remains cost-effective, it is also the most emissions-intensive.

Divergence in standards on what constitutes low-carbon concrete and steel

Decarbonising concrete and steel production is critical to achieving national and global climate goals, and low-carbon alternatives to conventional production already exist. Low-carbon pathways to concrete production include: (i)reducing conventional Portland cement use by substituting with low-carbon alternatives or supplementary cementitious materials or using recycled aggregates (iii)fuel-switching to cleaner energy sources to reduce fossil fuel consumption. (iii)Deploying carbon mineralisation technologies to lower emissions intensity in the concrete manufacturing process. For steel, significant emission reductions can be achieved through increased adoption of technologies such as Direct Reduced Iron (DRI) and Electric Arc Furnace (EAF). Using scrap or recycled steel is another key lever for reducing emissions from the steelmaking process.

Source: World Steel Association

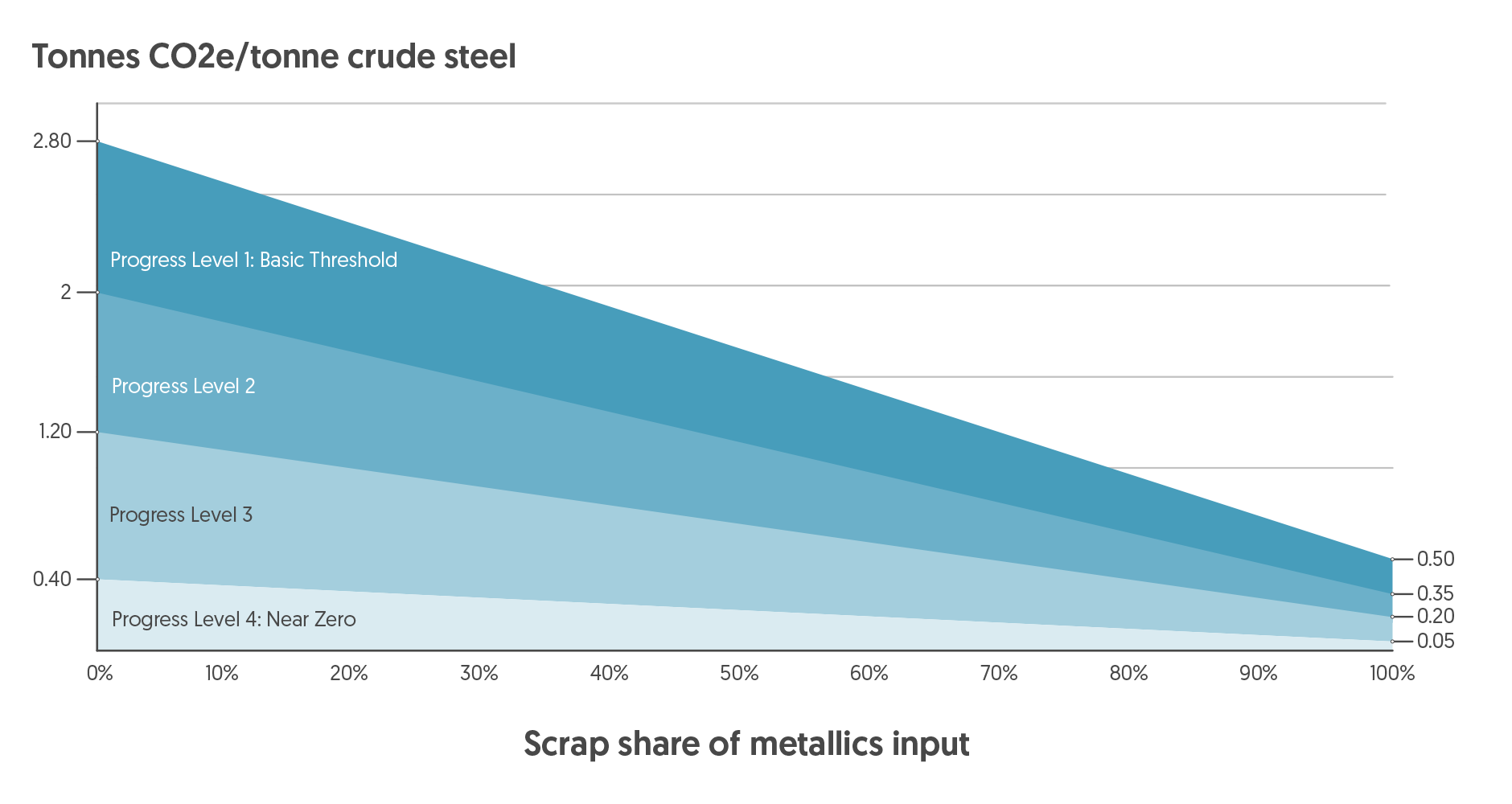

However, there is currently little consensus on what it means for concrete and steel to be considered ‘green’. Key indicators of green concrete have shifted from more prescriptive metrics e.g. % of recycled or clinker content, towards performance-based metrics e.g. carbon emissions intensity. For example, the Singapore Green Building Council (SGBC)’s Singapore Green Building Product (SGBP) Certification for Ready-Mix Concrete previously rated products based on clinker content but has recently changed the criteria to Global Warming Potential (GWP) measured in kgCO2e/m3 volume of concrete. However, even if emissions intensity is used as a common metric, the thresholds for what is considered ‘green’ vary across markets. For example, Hong Kong Construction Industry Council’s (CIC) Green Product Certification considers concrete to be ‘best-in-class’ if it produces less than 206 – 375 kgCO2e/m3, while the Global Cement and Concrete Association’s Global Ratings for Concrete has much stricter guidelines: to earn an A-grade or better rating, concrete must produce less than 68 – 113 kgCO2e/m3, depending on the concrete strength grade. The thresholds used by different green product certification bodies and industry initiatives vary, as they cater to regional differences in material sources and conditions of production decarbonisation progress on a rating scale of Level 1 (basic) to Level 4 (near -zero), while considering the variable amounts of scrap used in steel production.

Similarly, for green steel, some adopt a stricter definition of ‘steel manufactured without the use of fossil fuels’, while others use the term ‘green steel’ or ‘low-carbon steel’ interchangeably to refer to steel produced with significantly lower emissions than BF-BOF (such as natural-gas based DRI-EAF). Globally, there is a proliferation of standards and initiatives attempting to define what low-carbon steelmaking means. For example, ResponsibleSteel, the industry’s first global standard and certification programme, uses a ‘sliding-scale approach’ (see Figure below), which assesses the level of decarbonisation progress on a rating scale of Level 1 (basic) to Level 4 (near-zero), while considering the variable amounts of scrap used in steel production.

Source: Responsible Steel International Production Standard Version 2.1

In the finance sector, the EU Taxonomy for Sustainable Activities uses emission intensity (tCO2e/t product) thresholds as a key metric to define what is ‘green’ steel, although these thresholds do not vary based on scrap volume. In the end-use sectors, Ste elZero (a corporate initiative aimed at boosting demand for low carbon steel) adopts ResponsibleSteel’s ratings, but also includes ‘steel produced by a steelmaker with a science-based emissions target’ in its definition of ‘lower emission steel’, signalling acceptance of forward-looking emissions targets rather than actual performance.

The lack of harmonised definitions for green concrete or steel often creates confusion for contractors or project owners making purchasing decisions. Recognising this challenge, the industry is increasing efforts to enhance alignment and enable interoperability between frameworks and standards. One recent example is the agreements announced at COP30 in Belem, Brazil between ResponsibleSteel, the China Iron and Steel Association (CISA) and Europe’s Low Emission Steel Standard (LESS). The three organisations collectively cover around 60% of the world’s steel production, and the agreements are aimed at advancing global comparability and trade in low-carbon steel.

Price premium of green materials

The price premium for green materials remains a key barrier to adoption in the built environment, in addition to the lack of consensus on clear definitions and standards. The International Energy Agency (IEA) estimates that the production costs of near-zero crude steel carry a 10% to 75% premium compared to conventional crude steel production costs at present, varying with technology types and regional factors such as energy and labour costs. This translates to approximately US$225/t of crude steel in 2030, which is a 40% premium compared to current conventional crude steel.

Similarly, the production cost of near-zero cement will typically carry a premium of 30% to 125% compared to current conventional cement production costs, depending on regional and technological factors. This translates to an average premium of US$60/t of cement globally, which is 75% higher than current conventional cement. This implies that for concrete, the premium is likely to be lower, since cement accounts for a portion of concrete production costs and it can be substituted with other supplementary cementitious products. However, low-carbon concrete is still estimated to carry a 15% to 40% premium and this range differs across markets.

While some buyers have indicated a willingness to purchase low-carbon materials in the built environment, they are unable to do so due to insufficient availability on the market. These buyers do not have the scale to generate strong demand signals and are unable to take on the full risk needed to establish robust markets for green materials. Certain buyers may only be willing to partially cover the price premium, thereby requiring support through other means to close the gap. On the other hand, it may be difficult for suppliers to justify upfront CAPEX investments needed for low-carbon materials production without certainty in demand and offtake price. To bridge the price gap, government-led measures can alleviate some of the risk and cost burden faced by early movers.

Policies and regulations driving the built environment’s low-carbon transition

1. EU Carbon Border Adjustment Mechanism (CBAM)

The EU introduced CBAM in 2023 as a climate policy designed to level the playing field between the EU and third-country producers, by putting a fair price on carbon on certain imported products (including cement and steel) while phasing out free allocation of emissions allowances to the European industry. The EU CBAM is a carbon leakage instrument that functions in tandem with the EU Emissions Trading System (EU ETS), that requires EU importers to purchase CBAM certificates equivalent to the weekly average auction price of EU allowances.

During the EU CBAM’s transitional phase (2023–2025), importers of goods in the scope had to report their emissions embedded in their imports and did not have to buy and surrender CBAM certificates. The EU CBAM entered its definitive regime on 1 Jan 2026, where EU importers will have to declare their emissions embedded in their imports and pay a levy on certain products e.g. cement and steel.

Cement and steel producers that export products to the EU face the choice of paying higher carbon costs or reducing carbon emissions embedded in their products. The EU CBAM thereby incentivises the industry to produce low-carbon cement and steel to reduce carbon costs, as low-carbon cement and steel.

2. China Emissions Trading System (ETS)

China, the single largest producing country for both cement and steel, is also introducing carbon pricing to curb emissions from the production of these two materials. Prior to 2024, China’s ETS only included the power sector. In 2024 (following the introduction of EU CBAM), China’s Ministry of Ecology and Environment (MEE) announced the expansion of the national ETS to the aluminium, steel and cement sectors.

According to the latest work plan released by MEE, in 2026 and 2027, companies in the new sectors need to pay retrospectively for their emissions incurred in 2025 and 2026 respectively. In the initial years, companies will be given free China Emission Allowances (CEAs) that do not deviate too much from their actual emissions, limiting any immediate impact on the cost of production. However, MEE said that the carbon intensity benchmarks will be gradually tightened from 2028 onwards, which is expected to make it tougher for low-efficiency producers to survive in a highly competitive market with overcapacity issues. Carbon pricing mechanisms such as the China ETS can also increasingly bridge the price gap between low-carbon and emissions-intensive production, largely by increasing the cost of conventional and higher-emitting production.

3. Building Sector Policies and Standards

The building and construction sector is the single largest end-use sector for cement and steel, consuming about 50% of total steel (World Steel Association) and vast majority of total cement produced. Embodied carbon policies in the sector play a key role in shaping the demand for low-carbon concrete and steel. Currently, embodied carbon regulatory policies differ across markets, depending on the capacity and maturity of the local industry.

Several countries have mandated or proposed embodied carbon reporting for the building and construction sector as part of their climate-related disclosure regulations. For example, from 2028, all EU member states must report embodied carbon for major construction projects. This requirement will be extended to all projects by 2030, together with the introduction of specific embodied carbon limits. Some countries incorporate embodied carbon assessments and reporting in their legislation and building code. For example, Denmark has introduced carbon limits for new buildings (including embodied carbon emissions) since 2023. In Singapore, it is mandatory for developers to address embodied carbon emissions as part of the Code for Environmental Sustainability of Buildings.

Apart from national-level policies, several green building standards globally have started incorporating embodied carbon as part of their certification requirements. For example, Green Star Buildings has a minimum expectation on projects to have 10% less upfront carbon emissions compared to a standard building from materials. For BREEAM New Construction, in order to attain higher ratings of ‘Excellent’ and ‘Outstanding’, project-stage lifecycle assessment and embodied carbon reporting are required. Other standards have target thresholds of embodied carbon performance where attainment allows for points to be awarded. For example, in LEED certification criteria, projects can earn credits based on their ability to reduce GWP. In Singapore’s Green Mark’s Whole Life Carbon section, additional points can be scored when project teams report and promote the reduction of whole life carbon in their projects. Various calculation tools have also been developed to support embodied carbon reporting, such as the Embodied Carbon in Construction Calculator (EC3) tool, Singapore Building Carbon Calculator (SBCC) and NABERS Embodied Carbon tool.

Looking ahead

Scaling markets for low-carbon cement and steel can contribute to achieving global climate goals. The pace and success of the cement and steel sectors’ transition to low-carbon pathways will be shaped by factors including:

- Technological advancements that enable scalable low-carbon solutions, such as carbon capture utilisation and storage (CCUS) and commercially available low-carbon hydrogen for steel and cement production;

- Increasing alignment and enabling interoperability between frameworks and standards for low-carbon materials;

- The degree to which major end-use sectors, in particular buildings and infrastructure, prioritise reducing embodied carbon; and

- The evolution of carbon pricing mechanisms across both producing and purchasing countries, and how this can bridge the price gap between conventional and low-carbon materials.

The transition to low-carbon cement and steel could trigger a reshaping of the global supply chain for building materials. New manufacturing hubs are also emerging, such as those in the Middle East leveraging abundant natural gas as a cost advantage to produce DRI. Understanding the interdependencies among these factors is critical for assessing potential pathways and investment opportunities in these key industries.

Important information

This advertisement has not been reviewed by the Monetary Authority of Singapore. General Disclaimers Foreign Currency Global Equities Disclaimer Dual Currency Returns Collective Investment Schemes Cross Border Market Disclaimers