Michael Tan

Senior Investment Counsellor, Wealth Management Singapore, OCBC Bank

Member of OCBC Wealth Panel

Working adults should start saving for their retirement early, to beat rising costs and enjoy their golden years

LIKE many Singaporeans, OCBC Wealth Panelist Michael Tan envisions an idyllic life as a retiree. With the money he has saved over the years, his family will be well-taken care of, giving him and his wife the time and finances to pursue interests they are both passionate about.

The senior investment counsellor, Wealth Management, at OCBC Bank, adds that he is nearing retirement, and so, is mulling over extended holidays, learning new skills and doing charity work. He says: "I am not musically inclined, but my wife and I learnt to play drums for a year. We could continue with this. It is therapeutic, exciting and invigorating to learn new things." Mr Tan would also like to spend time in a new country to see it through the eyes of a local, as well as relearn the Malay language he used as a young man living in a kampung.

Planning is key

That said, working gives Mr Tan a lot of satisfaction, even though retirement is looming for the 54-year old. "I encourage everyone to continue working for as long as they are able," he says. And as many savvy savers and investors know, people need to plan their finances in order to achieve a comfortable retirement.

Before considering that, however, they need to ensure that their expenditure is lower than their income. He says: "The reality is that, when it comes to retirement, the only certainty is uncertainty. Without some form of savings, you are unable to plan even for month-to-month, much less the future. As our society continues to live longer, one consideration is also to make sure you do not outlive your retirement monies." To be prepared for uncertainties like health and financial shocks, Mr Tan recommends setting aside a small amount of money every month.

"As our society continues to live longer, one consideration is also to make sure you do not outlive your retirement monies. On the whole, one should consider how to live out his retirement years. "Whether you travel, live with your children or support a charity, the activities you engage in influence your financial planning," he explains.

Planning for the next generation is just as important to Mr Tan, who has a child aged 26. "Anyone, not just the rich, can make a difference to their family financially with a well-thought out plan. You can also make a will," he says.

Saving early

Mr Tan recommends planning your retirement as soon as possible, "when you start your first job".

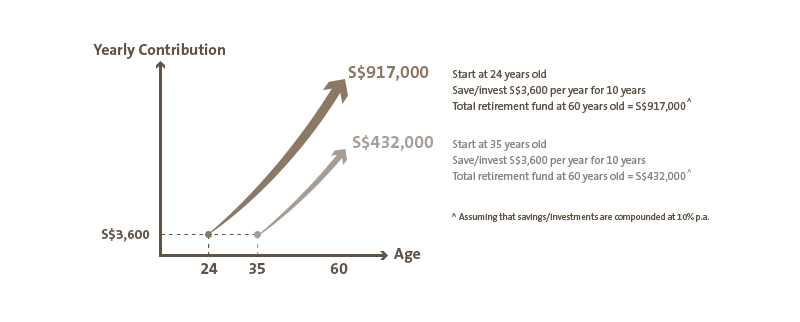

He says: "Inflation is an insidious beast. However, if you compound your savings or investment at an appropriate rate, you will be able to slay this mighty beast. "For example, if you are 24 years old, and you save or invest $3,600 a year for 10 years and it is compounded at 10 per cent per annum, you should have about $917,000 when you reach 60 years of age," says Mr Tan. "You would only have amassed $432,000 when you reach 60, if you were to start saving for your retirement at 35," he adds.

"Many of us remember that in the 1970s, the price of a three-room HDB flat was about $7,000. It now costs about $300,000 to $400,000, even with a shorter lease than when it was new." He also mentions the possibility of dealing with medical expenses, citing the case of cancer patients, who may face chemotherapy and traditional Chinese medicine treatment fees of up to $400,000 currently. He adds: "Retirement planning is a continuous process where you revisit your plans regularly. This is to adjust for changes in life and circumstances."

Mr Tan notes that current government schemes to help Singaporeans save for their old age - such as the Central Provident Fund (CPF) - can provide for just a minimum standard of retirement life. Furthermore, old age may come with unexpected health expenses, which may prove more of a burden during what are meant to be one's golden years.

"You should manage your cash flow, safeguard your future against unfortunate or unexpected or unforeseen events and invest for the very long term to ensure a comfortable and peaceful retirement", says Mr Tan. "You are always working towards the day when you decide to work only because you want to, not because you have to."

That something extra

To those planning for their retirement, he recommends considering various investment assets and insurance schemes to supplement CPF and Supplementary Retirement Scheme (SRS) savings. "We have to consider all assets and their planned use for and during our retirement. A house's rental income can contribute to one's retirement monies as well," he explains. "Medishield Life helps you to cover your basic hospitalisation costs, but it is important to supplement with critical illness, disability and life insurance to ensure a more comprehensive coverage," he adds.

OCBC's PremierLife Generation scheme can assist individuals in meeting their retirement and wealth transfer needs.Apart from helping you prepare financially for your retirement, the policy also ensures wealth transfer for up to three family generations.

PremierLife Generation is a Singapore-dollar denominated, single-premium insurance plan that guarantees a monthly payout from the fifth year onwards, supplementing your retirement plans with a regular income. The minimum single premium for the plan stands at $100,000. The policy can also be transferred to your child when he or she turns 18. On the demise of your child, your grandchild would receive a lumpsum payout from the policy.

"Success does not come easy. It would have taken years of sacrifice, perseverance and hard work to get where you are today," says Mr Tan. "You want to ensure that your family and future descendants can continue to enjoy the benefits of your hard-earned wealth."

Retirement must-dos

- Make sure your spending is lower than your income;

- You should start retirement planning as soon as possible;

- Compound your savings or investments early at an appropriate rate;

- Invest for the very long term to ensure a comfortable and peaceful retirement;

- Consider all your assets and their planned use for and during your retirement; and

- Manage your cash flow and safeguard your future against unfortunate, unexpected or unforeseen events.

Investment recommendation

At OCBC Premier Banking, both customers and Premier Banking Relationship Managers have access to rich market information provided by the OCBC Wealth Panel. With over 200 years of collective investment experience, the Panel's insights are available to help guide customers' investment decisions.

This is the bank's recommendation:

- PremierLife Generation

Important Information

Any opinions or views of third parties expressed in this material are those of the third parties identified, and not those of OCBC Bank. The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Before you make any investment decision, please seek advice from your OCBC Relationship Manager regarding the suitability off any investment product taking into account your specific investment objectives, financial situation or particular needs. In the event that you choose not to seek advice from your OCBC Relationship Manager, you should carefully consider whether the product is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into any transaction or to participate in any particular trading or investment strategy. OCBC Bank, its related companies, their respective directors and/or employees (collectively Related Persons') may have positions in, and may effect transaction in the products mentioned herein. OCBC Bank may have alliances with the product providers, for which OCBC Bank may receive a fee. Product providers may also be Related Persons, who may be receiving fees from investors. OCBC Bank and the Related Person may also perform or seek to perform broking and other financial services for the product providers.

The information in this material is not intended to constitute research analysis or recommendation and should not be treated as such.

The contents of this material are a summary of the investment ideas and recommendations set out in OCBC Investment Research and Group Treasury research reports. Please refer to the respective research report for the interest that the entity might have in the investment products and/ or issuers of the securities.

Foreign currency investments or deposits are subject to inherent exchange rate fluctuation that may provide opportunities and risks. Earnings on foreign currency investments or deposits would be dependent on the exchange rates prevalent at the time of their maturity if any conversion takes place. Exchange controls may be applicable from time to time to certain foreign currencies. Any pre-termination costs will be deducted from your deposit.

For fund investments, a copy of the prospectus of each fund is available and may be obtained from the relevant fund manager or any of its approved distributors. You should read the prospectus for details on the relevant fund before deciding whether to subscribe for, or purchase units in the fund. The value of the units in the funds and the income accruing to the units, if any, may fall or rise. Please refer to the prospectus of the relevant fund for the name of the fund manager and the investment objectives of the fund.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent.

Cross-Border Marketing Disclaimer

1. Indonesia: The offering of the investment product in reliance of this document is not registered under the Indonesian Capital Market Law and its implementing regulations, and is not intended to constitute a public offering of securities under the Indonesian Capital Market Law and its implementing regulations. The investment product may not be offered or sold, directly or indirectly, within Indonesia or to citizens (wherever they are domiciled or located), entities or residents, in any manner which constitutes a public offering of securities under the Indonesian Capital Market Law and its implementing regulations.

2. Malaysia: Oversea-Chinese Banking Corporation Limited (?OCBC Bank?) does not hold any licence, registration or approval to carry on any regulated business in Malaysia (including but not limited to any businesses regulated under the Capital Markets & Services Act 2007 of Malaysia), nor does it hold itself out as carrying on or purport to carry on any such business in Malaysia. Any services provided by OCBC Bank to residents of Malaysia are provided solely on an offshore basis from outside Malaysia, either as a result of ?reverse enquiry? on the part of the Malaysian residents or where OCBC Bank has been retained outside Malaysia to provide such services. As an integral part of the provision of such services from outside Malaysia, OCBC Bank may from time to time make available to such residents documents and information making reference to capital markets products (for example, in connection with the provision of fund management or investment advisory services outside of Malaysia). Nothing in such documents or information is intended to be construed as or constitute the making available of, or an offer or invitation to subscribe for or purchase any such capital markets product.

3. Myanmar: OCBC Bank does not hold any licence or registration under the FIML or other Myanmar legislation to carry on, nor do they purport to carry on, any regulated activity in Myanmar. All activities relating to the client are conducted strictly on an offshore basis. The customers shall ensure that it is their responsibility to comply with all applicable local laws before entering into discussion or contracts with the Bank.

4. Taiwan: The provision of the information and the offer of the service concerned herewith have not been and will not be registered with the Financial Supervisory Commission of Taiwan pursuant to relevant laws and regulations of Taiwan and may not be provided or offered in Taiwan or in circumstances which requires a prior registration or approval of the Financial Supervisory Commission of Taiwan. No person or entity in Taiwan has been authorised to provide the information and to offer the service in Taiwan.

5. Thailand: Please note that OCBC Bank does not maintain any licences, authorisations or registrations in Thailand nor is any of the material and information contained, or the relevant securities or products specified herein approved or registered in Thailand. Interests in the relevant securities or products may not be offered or sold within Thailand. The attached information has been provided at your request for informational purposes only and shall not be copied or redistributed to any other person without the prior consent of OCBC Bank or its relevant entities and in no way constitutes an offer, solicitation, advertisement or advice of, or in relation to, the relevant securities or products by OCBC Bank or any other entities in OCBC Bank?s group in Thailand.

6. Hong Kong SAR: This document is for information only and is not intended for anyone other than the recipient. It has not been reviewed by any regulatory authority in Hong Kong. It is not an offer or a solicitation to deal in any of the financial products referred to herein or to enter into any legal relations, nor an advice or a recommendation with respect to such financial products. It does not have regard to the specific investment objectives, financial situation and the particular needs of any recipient or Investor. This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without OCBC Bank?s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates to any registration, licensing or other requirements within such jurisdiction.

? Copyright 2016 - OCBC Bank | All Rights Reserved. Co. Reg. No.: 193200032W