Group CFO’s Overview

Ms Goh Chin Yee

Group Chief Financial Officer

Profit before tax rose 2% to a new high of $9.12 billion in 2025, supported by record total income amid a declining interest rate environment, underscoring the Group's diversified income streams. Net profit was 2% lower than a year ago due to higher income tax expenses from increased profit contribution from higher tax jurisdictions, and implementation of Base Erosion and Profit Shifting (BEPS) Pillar Two which requires a top-up to 15% minimum global tax for each jurisdiction from 1 January 2025.

The Group's record income was driven by strong broad-based growth in non-interest income, which more than offset the lower net interest income as key benchmark rates declined significantly. Softer net interest income was cushioned by sustained loan growth, proactive funding cost and balance sheet management, including the deployment of excess liquidity to income-accretive high-quality assets. Non-interest income surged 16% to $5.46 billion, boosted by robust 33% growth in wealth management fees to a new high, and double-digit growth in trading and insurance income. This broad-based uplift reflects the strength of our integrated financial services model in capturing customer flows across market cycles.

Loans grew by a healthy 9% to $341 billion on a constant currency basis, contributed by both corporate and consumer segments, and driven by the Group's key regional and international markets. In particular, we increased lending to customers in key growth sectors such as renewable energy, technology, media and telecommunications (TMT) including digital infrastructure, transport and Singapore residential mortgages. Sustainable financing loans grew 13% to $56.5 billion and accounted for 17% of Group loans, while total commitments stood at $80 billion.

Customer deposits rose 10% from a year ago, driven by CASA deposit growth across consumer, SME and corporate segments, and lifted CASA ratio to nearly 51%.

Asset quality stayed resilient as we remained prudent in our risk management. Non-performing loan ratio was stable at 0.9%. Total allowances were 4% lower, and credit costs declined to 17 basis points from 19 basis points a year ago. Non-performing assets coverage ratio was 151%.

While we continued investing in strategic initiatives to drive business expansion, and in talent development and technology to support growth, costs were well controlled with cost-to-income ratio remaining at 40%.

Our balance sheet stayed robust. Funding, capital and liquidity positions were well above regulatory requirements. Common Equity Tier 1 Capital Adequacy Ratio (CET1 CAR) stood at 16.9% as at 31 December 2025 on a transitional basis upon adoption of MAS' final Basel III reform rules from 1 July 2024. On a fully phased-in basis, our CET1 CAR was 15.1%.

Amid global uncertainties, market volatility and declining interest rates, our resilient performance underscores the strengths of our diversified franchise and disciplined financial management.

Driving Shareholder Returns

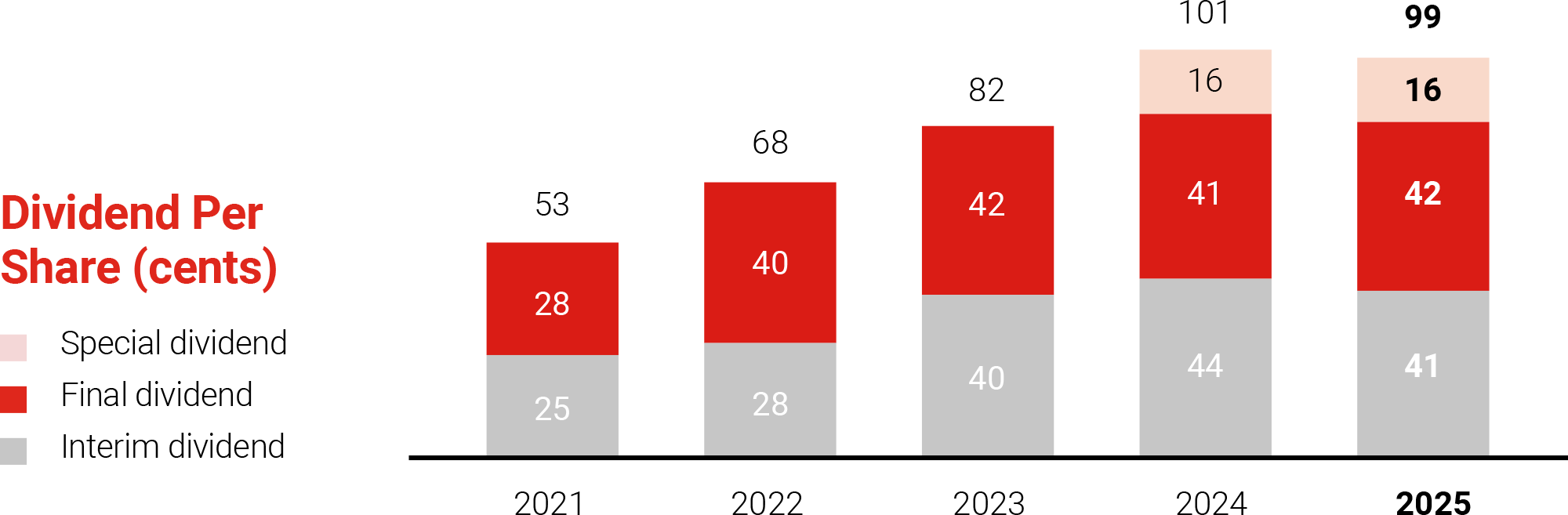

We remain guided by our dividend policy to pay out 50% of the Group s core net profit to shareholders. We exceeded this target, paying out 53% in 2022 and 2023.

Dividend payouts were raised to 60% in 2024 and 2025 – part of a $2.5 billion two-year capital return plan announced in February 2025. We are committed to completing the capital return plan by financial year 2026.

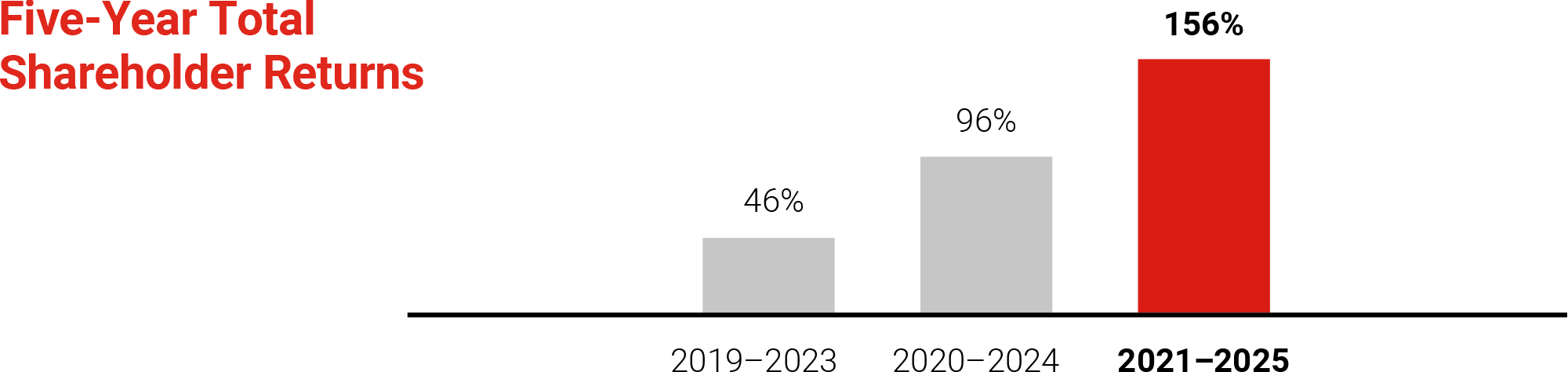

Our strong balance sheet and capital position have enabled us to deliver higher shareholder returns. Our five-year total shareholder returns rose to 156%, from 96% in the previous year. This has reinforced conviction in our ability to consistently deliver long-term value for shareholders.

Robust Funding Base

OCBC continued to maintain a healthy funding position, supported by strong customer deposits franchise and supplemented by diversified funding options. In 2025, we issued a A$1 billion Australian Medium Term Note (AMTN) in January, and EUR 500 million in fixed rate covered bonds under our US$10 billion Global Covered Bond Programme in April. We issued a benchmark AMTN green bond in August, the first by a financial institution in 2025, and a US$1 billion Tier 2 issuance under our US$30 billion Global MTN Programme in September.

Looking Ahead to 2026

Our 2025 results attest to the commitment and effort of everyone across the OCBC Group. I would also like to thank our global investor community. We look forward to deepening engagement and providing even greater clarity on our strategic priorities.

The 2026 outlook remains uncertain amid continued geopolitical tensions. That said, our key markets have demonstrated resilience, and we are confident of their prospects. In addition, our new corporate strategy positions us well to capture growth, and our strong capital position enables us to navigate the challenges. We will remain disciplined in balancing these considerations with delivering sustainable long-term shareholder returns.

We are increasing our focus on returns and maintaining efficient cost of capital to support sustainable business expansion. We will allocate capital purposefully to higher-return businesses and other areas that matter most, particularly investments in AI, Digital and Data – capabilities that anchor our corporate strategy – to drive long-term competitiveness and deliver enduring value.