Group CEO’s Perspectives

Mr Tan Teck Long

Group Chief Executive Officer

At the same time, interest rates began to come down in several markets after a prolonged period of tight monetary conditions. In Hong Kong, sharp movements linked to the HIBOR episode highlighted how sensitive financial markets remain to changes in liquidity and confidence. Alongside these developments, AI moved rapidly from experimentation to everyday use, changing how people work, how businesses operate and how customers expect to be served.

In this environment, we stayed focused on the fundamentals. We safeguarded our customers' interests, supported businesses through changing macroeconomic conditions and made careful long-term investments. I am pleased to report another set of robust results. Our strong capital position, diversified businesses and disciplined risk management allowed us to navigate uncertainty while continuing to support the real economy across our key markets.

Overall Financial Performance

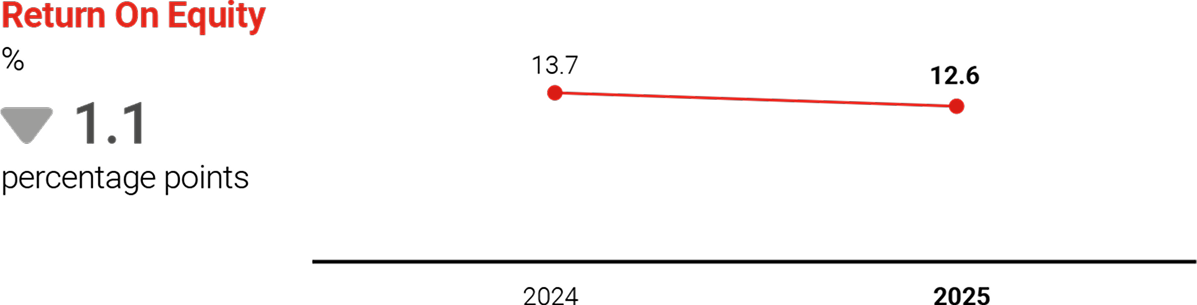

Our Group net profit for 2025 was $7.42 billion, moderately down by 2% from a year ago, while profit before tax rose 2% to a new high of $9.12 billion, despite a declining interest rate and challenging operating environment amid sustained macro uncertainties. This reflected the strength of OCBC Group's solid fundamentals, robust business franchise and ability to navigate through cycles.

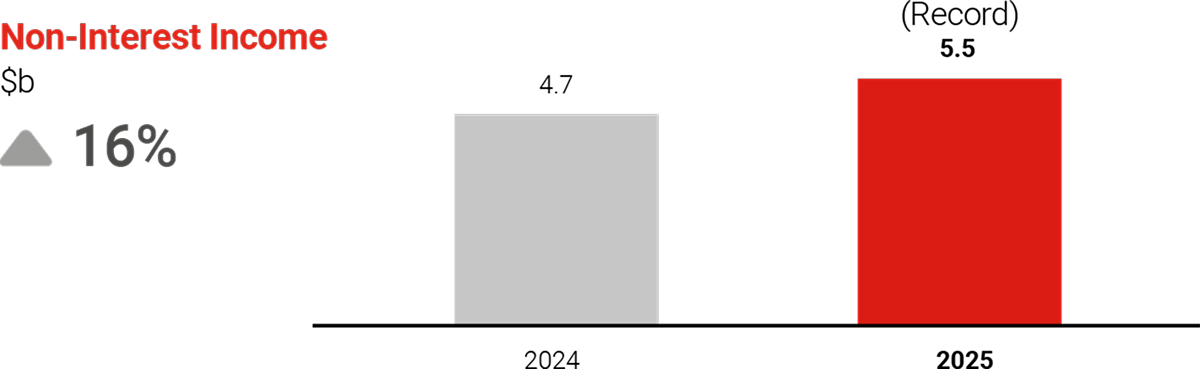

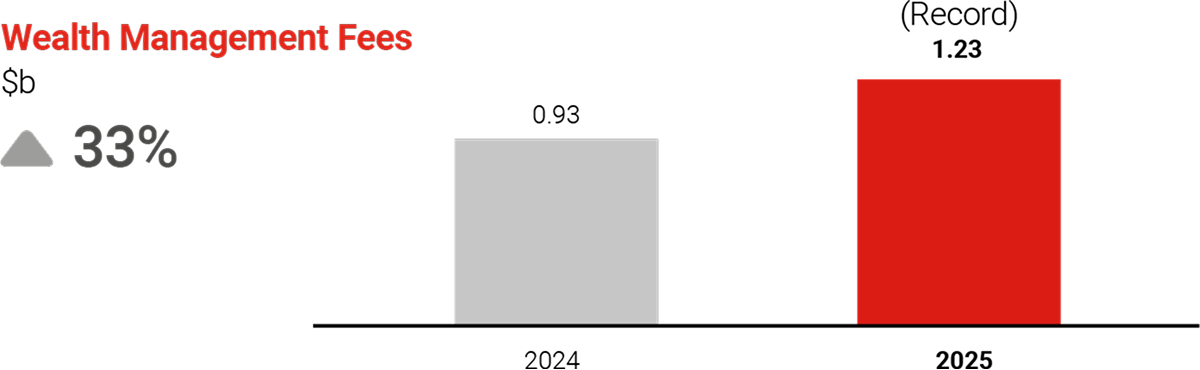

Total income rose to a record $14.6 billion despite headwinds from declining interest rates. We defended our net interest income with proactive balance sheet management while wealth, trading and insurance delivered stellar income for the year. Wealth management AUM and fee income hit record levels, which was a strong testament to our strategic efforts to drive growth in the wealth space.

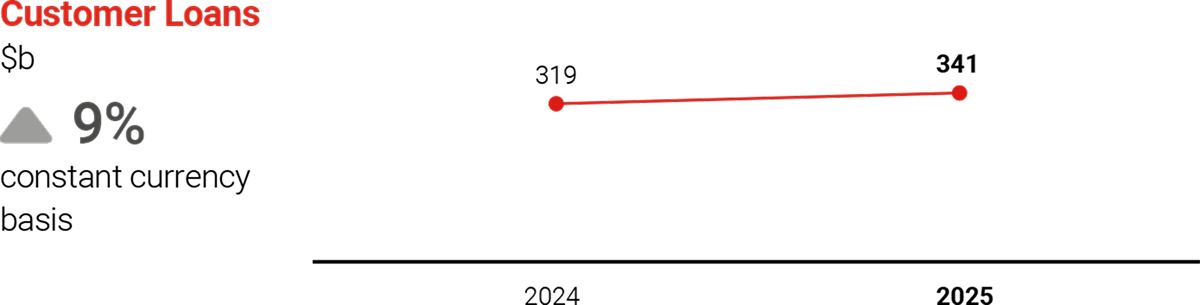

Loan growth momentum was sustained and our loan portfolio expanded at high single-digit for the second year. In 2025, loans grew 9% on a constant currency term, to $341 billion, driven by broad-based growth across industries. We are focused in capturing opportunities in key growth sectors including residential mortgages, renewable energy, technology, media and telecommunications (TMT) and infrastructure-related industries, while exercising prudent risk management and loan underwriting. Asset quality was sound with NPL ratio stable at 0.9% since mid-2024, and non-performing loan coverage stood at 151%.

Completing Our Current Strategy and Preparing for the Next Frontier

Since 2022, we have been executing our corporate strategy focused on strengthening our core franchises, deepening customer relationships and building the foundation across One Group. As we approach the final phase of this strategy, we are confident that these foundations are firmly in place. They have enabled us to deliver consistent performance, manage risks effectively and remain close to our customers through periods of uncertainty.

At the same time, we recognise that the next phase of growth will look different. The pace of change in technology, particularly in AI, is accelerating. Customer expectations and the business environment are also evolving just as quickly. As we close this chapter, we are deliberately pivoting towards a future where innovation and capability building play an even bigger role in how we create value.

Our New Corporate Strategy

Looking ahead, we have refreshed our corporate strategy to reflect a world that is becoming more complex, more digital and more interconnected. This strategy is anchored on several megatrends that are reshaping the operating environment for banks.

These include heightened geopolitical tensions that are changing trade and investment flows, shifting demographics that are redefining customer needs, the continued rise of Asian wealth, the rapid acceleration of AI and digitalisation, and the growing urgency of sustainability and climate transition.

Against this backdrop, our new strategy is designed to help OCBC ride these long-term waves and reposition the Group for the future. It is built around four broad strategic shifts.

First, an Asia shift, where we deepen our focus on Asia as a growth engine and strengthen connectivity within the region and beyond.

Second, a Tech shift, where we drive revenue through customer centricity enabled by AI, Digital and Data ("ADD") capabilities, and capture opportunities arising from digital infrastructure builds, accelerated by digitalisation and AI advancements.

Third, a Net-Zero shift, where we support the transition to a low-carbon economy while managing climate-related risks responsibly.

Fourth, a Franchise shift, where we sharpen our positioning and scale in core markets and customer segments.

These strategic priorities will be discussed in greater detail in the later sections of this Annual Report.

Staying the Course While Expanding Our Reach

Even as we prepare for the next phase, we remain disciplined in executing our strategy and strengthening our connectivity.

During the year, OCBC signed a Memorandum of Understanding with the UK Government's Office for Investment–the first such partnership between the Office and a Singapore bank to facilitate cross-border investments. This partnership positions OCBC to channel up to $17 billion of financing into priority UK sectors by 2030, including energy transition, infrastructure, data centres and real estate. It will also enable OCBC to support UK companies seeking to expand into Singapore and the broader Southeast Asian region.

Within ASEAN, we are well positioned given our long and significant presence on both sides of the causeway to support growth through the Johor-Singapore Special Economic Zone. OCBC has committed over RM15 billion in financing to businesses in Johor in less than two years, facilitating investments in manufacturing, real estate and data centres, and supporting cross-border supply chains and expansion.

Innovating to Create Long-Term Value

Innovation is central to how we serve our customers and run our businesses. We are embedding AI, digital and data across the Group to improve customer experience, strengthen risk management and raise productivity.

In Bank of Singapore, we deployed agentic AI to automate the preparation of source of wealth reports, improving turnaround times from 10 days to 1 hour, allowing relationship managers to accelerate client onboarding and periodic reviews.

Across our consumer and business banking platforms, we introduced secure in-app call capabilities, reducing fraud and enabling customers to connect with us seamlessly at the point of need while removing IDD charges and reducing scam risks. Our payments ecosystem also continued to expand, with OCBC now able to link to more than 10 payment wallets, simplifying domestic and cross-border payments.

We also advanced our blockchain journey by becoming the first bank in Singapore to issue bespoke tokenised bonds through our Asset Tokenisation Platform, building on blockchain infrastructure developed previously. To further strengthen USD liquidity resilience, we also established a US$1 billion digital commercial paper programme on blockchain, providing a new avenue for short-term funding.

Complementing these efforts, we deepened our research in quantum technologies through collaborations with NUS, NTU and SMU, the first time a bank has partnered all three universities, to explore applications in derivative pricing, data security and fraud detection.

A key milestone in this journey will be the opening of OCBC's presence in Punggol Digital District. We are excited to be part of this vibrant and energising new district, which brings together education, industry and technology innovation. Punggol Digital District will provide a strong platform for collaboration, digital talent development and experimentation, supporting the next stage of OCBC's transformation.

Investing in People, Communities and Sustainability

As demographics shift, supporting financial wellbeing across life stages is increasingly important. With Singapore approaching super aged status by 2026, our OCBC SeniorCare launch in March 2025 was timely. With over $2 million invested to support more than 180,000 seniors, the programme helps seniors manage their health, wealth, literacy and lifestyle needs with confidence. We introduced OCBC CARE Ambassadors in selected branches to assist seniors in familiar dialects and enhanced digital accessibility with smart text resizing on the OCBC mobile app.

As a leading SME bank, we expanded our key programmes regionally. Our Women Unlimited programme now extends across Singapore, Indonesia, Hong Kong and Malaysia, with a goal to support 10,000 women entrepreneurs by 2030. The Serial Entrepreneur programme, which supports founders who own multiple small businesses, was also expanded in 2025 across our core markets. This segment continues to grow, with one in three new businesses in Singapore started by an entrepreneur with an existing venture and almost half of the small businesses OCBC serves in Malaysia led by serial founders.

In partnership with Enterprise Singapore, we also launched the OCBC SME Start ESG Programme to help SMEs assess and improve their sustainability performance. The programme provides expert guidance, access to sustainability linked loans, and funding support for sustainability assessment costs to help SMEs build capabilities and stay competitive as global supply chains accelerate their net-zero commitments.

Strengthening Resilience for the Future

In an increasingly complex risk environment, organisational resilience is critical. We continue to strengthen our resilience capabilities to calibrate OCBC's position amid a continually evolving global landscape and to enhance the long-term sustainability of our businesses by seeking new growth engines.

This year marks an important leadership transition for the Group. We had key leadership changes, including Carina Lee (Group Chief Risk Officer), Melvyn Low (Group Chief Strategy and Transformation Officer) and Elaine Heng (Head of Global Commercial Banking). Their experience and leadership, together with the dedication of our Board, management team and employees, will help us build a strong foundation as we move forward.

Appreciation

2025's results are the outcome of the dedication and resilience of all our colleagues across OCBC Group. Their commitment to servicing customers, managing risks responsibly and executing our strategy has been central to OCBC's performance. I am also grateful to my management team and Board of Directors for the guidance and oversight.

2026 has begun amid heightened geopolitical uncertainties. As we navigate a more uncertain world, we believe the years ahead will continue to be shaped by digitalisation, changing trade patterns and the growing convergence of finance, technology and sustainability. OCBC enters The Next Frontier from a position of strength. We remain committed to building a bank that is trusted, innovative and resilient, creating long-term value for our customers, community and shareholders.

Mr Tan Teck Long

Group Chief Executive Officer

February 2026