OCBC Group First Quarter 2024 Net Profit Rose 22% from the Previous Quarter to a Record S$1.98 billion

OCBC Group First Quarter 2024 Net Profit Rose 22% from the Previous Quarter to a Record S$1.98 billion

The Group’s resilient quarter-on-quarter performance was driven by total income rising to a new quarterly high, strict cost discipline and lower allowances.

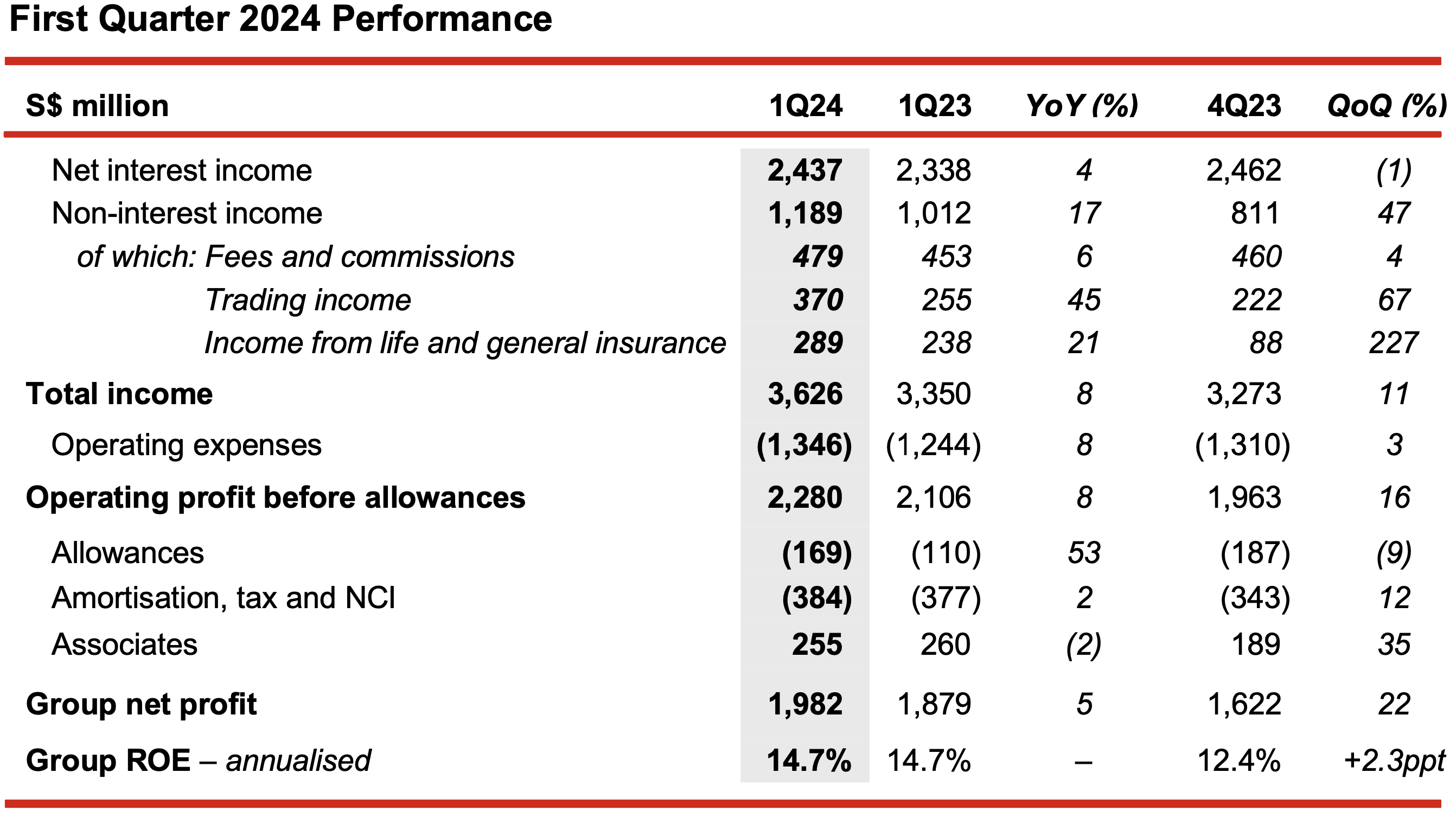

Singapore, 10 May 2024 – Oversea-Chinese Banking Corporation Limited (“OCBC”) reported net profit of S$1.98 billion for the first quarter of 2024 (“1Q24”), 22% higher than S$1.62 billion in the previous quarter (“4Q23”), and 5% above S$1.88 billion a year ago (“1Q23”).

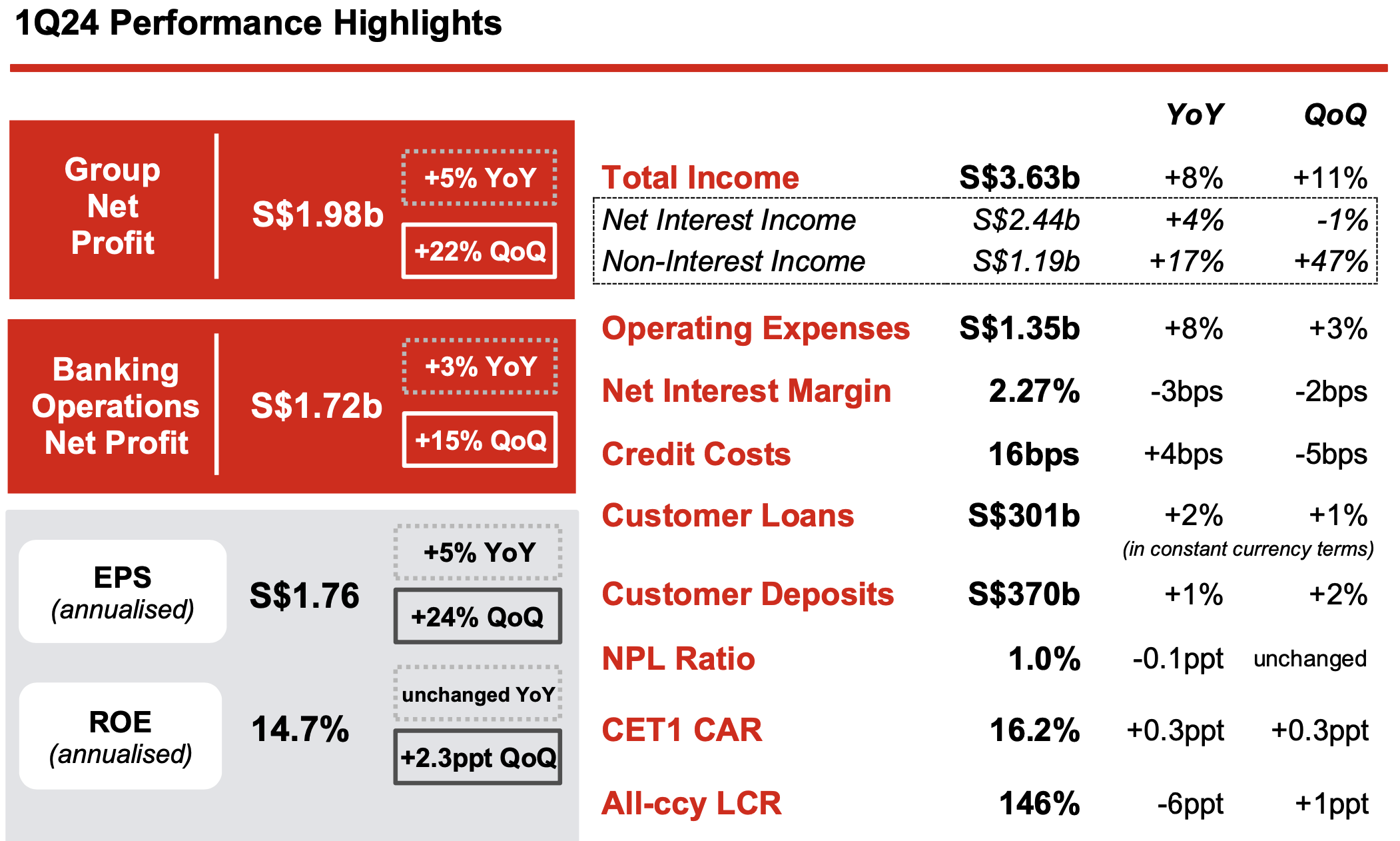

The Group’s resilient quarter-on-quarter performance was driven by total income rising to a new quarterly high, strict cost discipline and lower allowances. Income growth outpaced the increase in operating expenses, which drove an improvement in cost-to-income ratio (“CIR”) to 37.1%, while credit costs decreased to 16 basis points. Loans grew 1% and asset quality was sound with non-performing loan (“NPL”) ratio steady at 1.0%. The Group’s capital, funding and liquidity positions remained robust, providing flexibility to support business growth and handle uncertainties. Return on equity climbed to 14.7% and earnings per share was higher at S$1.76, on an annualised basis.

1Q24 Quarter-on-Quarter Performance

Group net profit rose 22% to S$1.98 billion, underpinned by record total income, well-controlled costs and lower allowances.

- Net interest income was S$2.44 billion, 1% below 4Q23’s record level, largely due to the effect of a comparatively shorter quarter. On a day-adjusted basis, net interest income was steady against the preceding quarter. Average assets grew by 1%, which largely compensated for a 2 basis-point moderation in net interest margin (“NIM”) to 2.27% as a rise in asset yields was outpaced by higher funding costs.

- Non-interest income rebounded by 47% to S$1.19 billion.

- Net fee income was S$479 million, 4% above the prior quarter. This was largely driven by an increase in wealth management, brokerage and fund management fees on the back of a rise in customer activities, as well as higher investment banking fees.

- Net trading income surged 67% to a new high, underpinned by record customer flow treasury income as well as improved non-customer flow treasury income.

- Insurance income was S$289 million, significantly higher as compared to S$88 million in 4Q23, supported by better investment performance and improvement in claims experience. Total weighted new sales grew 2% quarter-on-quarter to S$524 million, driven by higher single premium sales in Singapore, while new business embedded value (“NBEV”) was S$163 million.

- The Group’s wealth management income, comprising income from insurance, private banking, premier private client, premier banking, asset management and stockbroking, was a record S$1.29 billion, 33% above the previous quarter and contributed 36% to the Group’s total income. Group wealth management AUM was S$273 billion, up 4% from S$263 billion in the previous quarter.

- Operating expenses were S$1.35 billion, up 3% from a quarter ago, driven by higher staff costs from increase in variable compensation associated with income growth. The rise in expenses was outpaced by an 11% growth in total income, which drove CIR lower to 37.1%.

- Total allowances declined 9% from the prior quarter to S$169 million.

- Share of results of associates rose 35% to S$255 million, from S$189 million in 4Q23.

1Q24 Year-on-Year Performance

Group net profit increased 5% from a year ago, driven by an 8% rise in operating profit.

- Net interest income rose 4% from the previous year, led by a 5% growth in average assets, which more than compensated for a 3 basis-point decline in NIM, as rising funding costs offset the higher asset yields.

- Non-interest income was S$1.19 billion, 17% above the previous year, underpinned by improvement in fee, trading and insurance income.

- Operating expenses grew 8% from 1Q23 to S$1.35 billion, as the Group continued to invest in its franchise and people to support business expansion.

- Total allowances were S$169 million, higher as compared to S$110 million a year ago, mainly due to increased allowances for impaired assets.

- Share of results of associates of S$255 million was 2% below 1Q23.

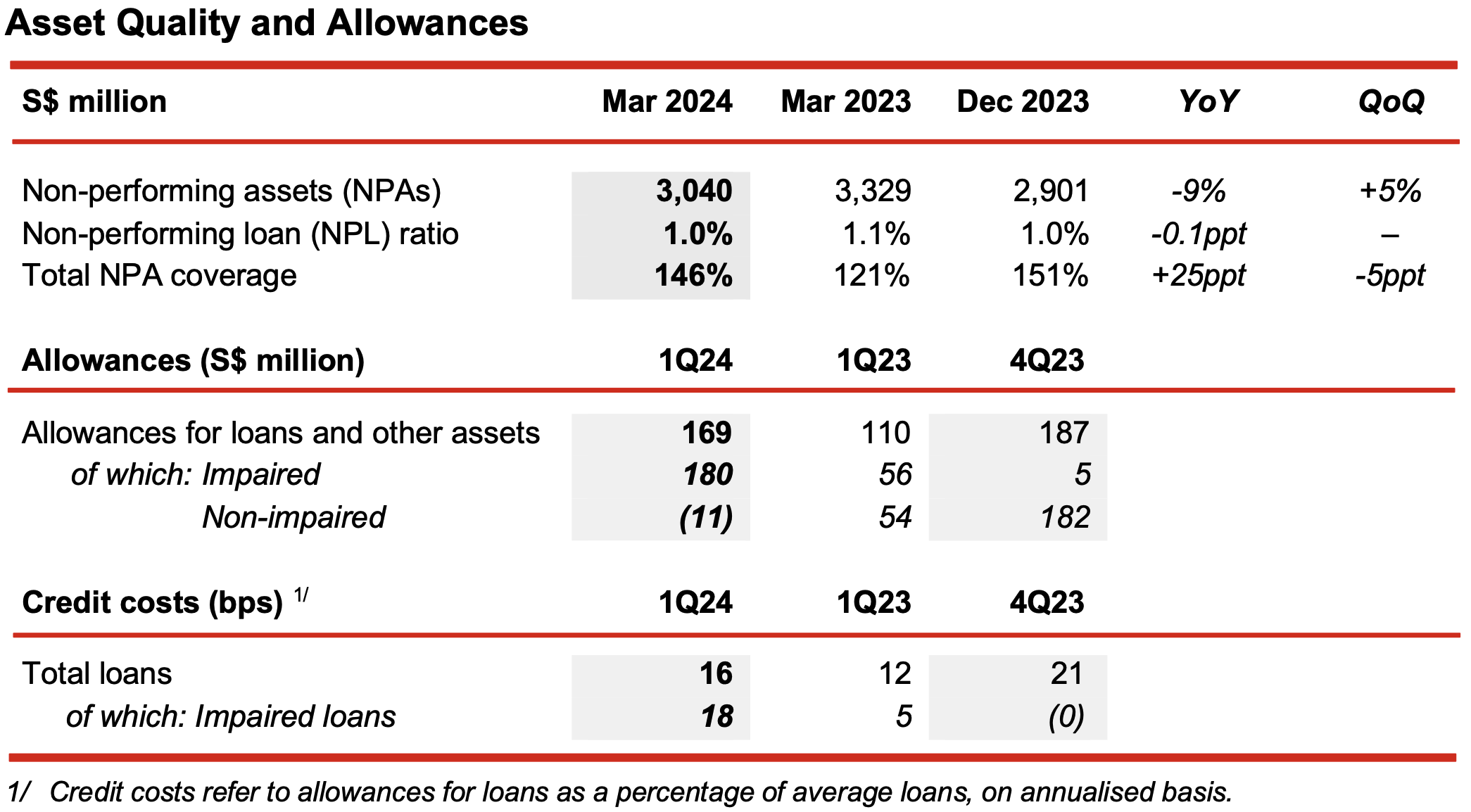

- Total NPAs were S$3.04 billion as at 31 March 2024, a drop of 9% from a year ago. Compared to the previous quarter, NPAs were 5% higher as net recoveries/ upgrades and write-offs were offset by new corporate NPA formation.

- NPL ratio was 1.0%, stable against the previous quarter and lower than 1.1% in the prior year. The allowance coverage for total NPAs was 146%.

- Total allowances were S$169 million in 1Q24. These comprised allowances for impaired assets of S$180 million, and write-back in allowances for non-impaired assets of S$11 million.

- Total credit costs for 1Q24 were an annualised 16 basis points.

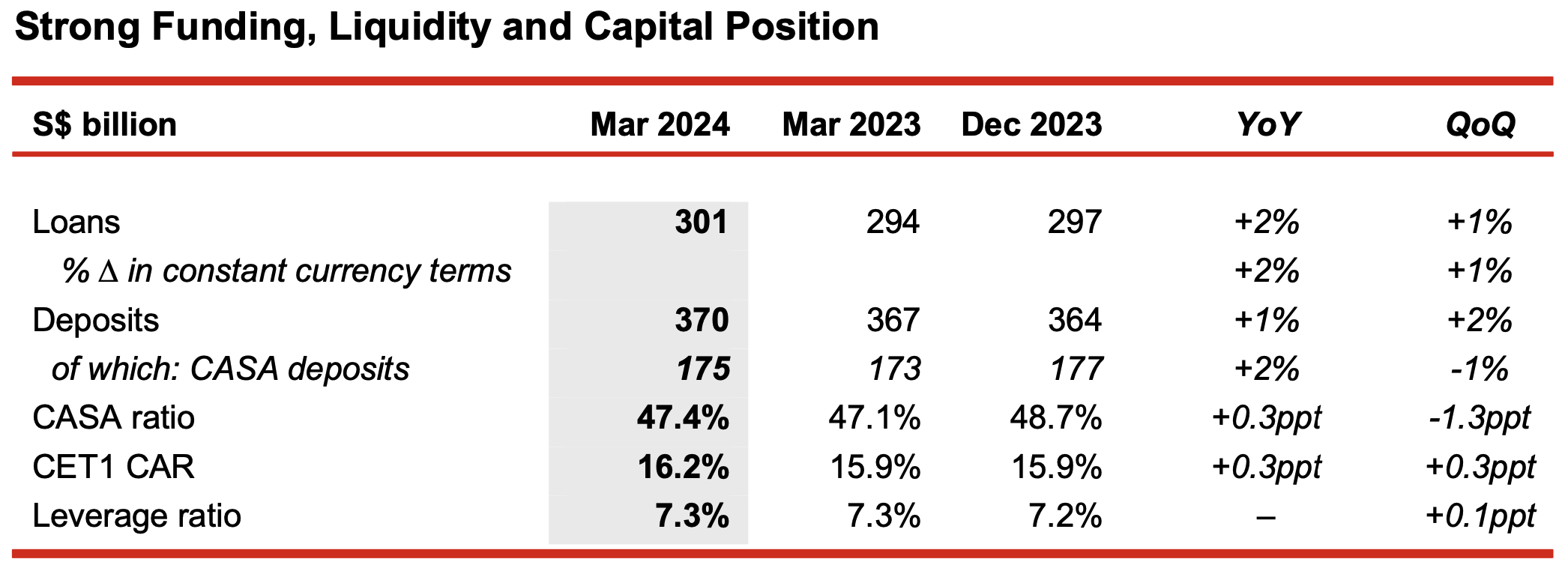

- Customer loans were S$301 billion as at 31 March 2024, up 2% from the previous year in constant currency terms. Compared to the prior quarter, customer loans were 1% higher.

- Loan growth of S$4 billion for the quarter was supported by an increase in both corporate and consumer loans. By geography, the expansion in loans was led by growth in Singapore.

- As at 31 March 2024, sustainable financing loans grew 34% from a year ago to S$43.1 billion, against a total loan commitment of S$60.5 billion.

- Customer deposits increased 1% quarter-on-quarter in constant currency terms to S$370 billion, in tandem with loan growth.

- Loans-to-deposits ratio was 80.3%, higher than 79.2% a year ago and comparable to 80.5% in the previous quarter.

- Group CET1 CAR was 16.2%, while the leverage ratio was 7.3%.

Message from Group CEO, Helen Wong

“We are pleased to start the year on a strong footing with robust first quarter results. We achieved record net profit which lifted return on equity higher, underpinned by income growth and strict cost discipline. Asset quality remained sound and we prudently maintained our credit allowances. Our performance was driven by the deep synergies across banking, wealth management and insurance. This demonstrates the ability of our diversified franchise to deliver resilient earnings growth towards achieving our strategic priorities.

While some recent economic indicators are looking more favourable, near-term risks remain, such as heightening geopolitical volatility arising from ongoing wars and the outcome of a number of key elections this year. Our key markets in Asia are expected to be resilient, benefitting from increasing capital flows and supply chain diversification. Our healthy balance sheet position provides us the flexibility to manage uncertainties, and capacity for growth as we continue to support our customers across our network.”