FX & Commodities

July 2026

Gold forecast lowered

We lower our gold and silver forecasts to reflect a tougher near-term macro setup, while keeping a mild upward-sloping path as the medium-term case remains intact.

Christopher Wong

Executive Director,

FX Strategist,

OCBC Group Research,

OCBC

Oil

Shipping activity—and, by extension, oil flows—through the Strait of Hormuz has recovered following the US-Iran memorandum of understanding. Vessel transits have rebounded to around 30% of normal levels, although the pace of recovery slowed after a container ship incident off the coast of Oman on 25 June. Much of the increase in traffic appears to reflect the release of floating storage that had previously been stranded in the Gulf. Meanwhile, weaker inbound traffic suggests shipowners remain cautious, implying that flows could moderate once the backlog of cargo has been cleared.

Expectations of a normalisation in oil flow have swiftly pushed crude prices back to pre-conflict levels, reviving the oversupply narrative. Physical market indicators also remain soft. Dated Brent continues to trade at a discount to futures prices, while the front end of the Brent curve has flattened. These signals point to a relatively loose near-term market, even as balances further along the curve remain tighter.

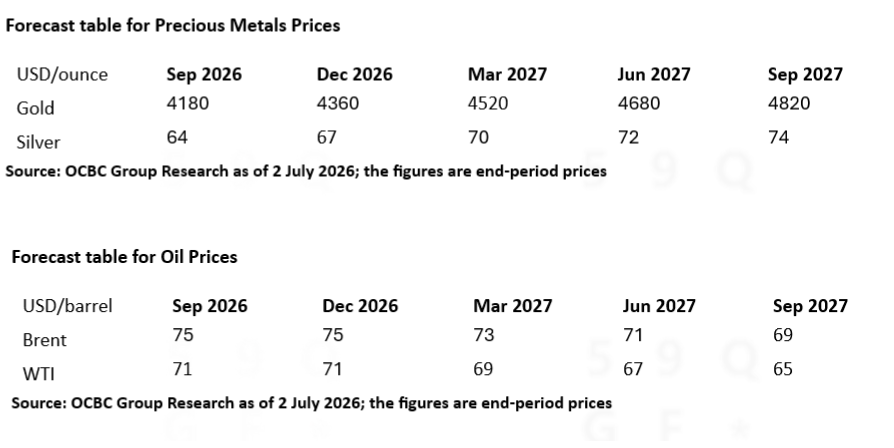

Against this backdrop, we lower our end-2026 Brent forecast to US$75/barrel from US$80/barrel and modestly reduce our 2027 outlook. Nevertheless, we expect the pace of further price declines to be limited, as markets may be overly optimistic about both the speed and durability of the supply recovery. De-mining operations in the Strait of Hormuz remain a key operational risk for shippers, while investors may also be underestimating the risk of renewed disruptions if the US–Iran ceasefire proves less durable than currently assumed.

In addition, strong US exports and weak Chinese imports helped contain the initial price spike but did so at the cost of lower inventories. As inventories are rebuilt, restocking demand from both economies should help absorb returning Middle East supplies and provide a degree of support to prices, even as the market adjusts to improved supply conditions.

Precious Metals

Gold

Gold came under renewed pressure in June as the macro backdrop turned less supportive. Real yields moved higher, the US Dollar (USD) strengthened, and Fed expectations shifted in a more hawkish direction. At the same time, ETF inflows eased following the strong buying seen earlier in the year. Together, these factors have made rallies more difficult to sustain, even though the medium-term investment case for gold remains intact.

In the near term, gold is likely to require at least one of three catalysts to regain momentum: lower real yields, a weaker USD, or a clearer unwinding of hawkish Fed expectations. Absent these developments, price action could remain choppy, with a period of consolidation below recent highs remaining a distinct possibility.

That said, we are not turning structurally bearish on gold. Ongoing central-bank reserve diversification, concerns over fiscal sustainability, geopolitical uncertainty, and continued demand for portfolio hedges should provide an important medium-term anchor for prices. However, these supportive factors may not fully insulate gold from further valuation adjustments if real yields and the USD remain elevated.

We have revised our gold price forecasts lower to reflect the more challenging near-term macro environment, while retaining an expectation of gradual gains over the medium term.

Silver

Silver also softened as the same macro headwinds facing gold, weighed more heavily on its higher-beta profile. Rising real yields, a stronger USD, weaker momentum in gold, and slower ETF inflows have reduced the marginal support that helped drive earlier gains.

The medium-term supply-deficit story remains intact, underpinned by demand from solar power, electrification, electronics, and the broader energy transition. However, the market appears less willing to reward these structural positives while the macro backdrop remains challenging. Silver's greater industrial exposure and more volatile investor base also mean that price corrections can be more pronounced when risk sentiment deteriorates or investor demand weakens.

In the near term, silver is likely to retain a softer bias until gold stabilises, real yields begin to ease, or ETF demand shows clearer signs of recovery. Until then, macro factors are likely to continue dominating the narrative over longer-term fundamentals.

We have revised our silver price forecasts lower to reflect this less favourable tactical environment, while continuing to expect a gradual recovery once macro conditions become more supportive.

Currency

US Dollar (USD)

Brent had retraced to pre-Iran conflict levels, reviving the pre-war oversupply narrative. Despite the deterioration in terms of trade from lower oil prices, the USD has strengthened. Support for the dollar has shifted from elevated oil prices to a more hawkish Fed and a flatter yield curve. With the Fed back in focus, the USD is realigning with interest rate differentials after the temporary dislocation caused by the energy shock.

Rising hawkish Fed risks have led us to shift our outlook from a rangebound USD to one of modest appreciation. At the same time, strong AI-driven equity performance is attracting capital back into US markets. We now forecast 2–3% USD appreciation by end-2026, revising our end-2026 EURUSD target to 1.11 (from 1.18) and USDJPY to 163 (from 155).

A move beyond 5% remains a tail risk and would likely require either oil prices rising above US$100/barrel or a re-acceleration of US growth rather than the soft-landing scenario currently expected. Carry trades should remain attractive as long as risk sentiment stays supportive, although funding currency selection will be increasingly important.

Japanese Yen (JPY)

Intervention risk is likely to limit USDJPY upside relative to other USD pairs, particularly in a stronger-dollar environment. Following approximately US$74bn of intervention between April and May, Japan's Ministry of Finance data show that the country still holds around US$1.3tn in FX reserves, highlighting its substantial capacity to intervene if needed. That said, intervention threats alone are unlikely to generate a sustained decline in the USDJPY.

The relationship between USDJPY and the US-Japan interest rate differential has weakened in recent years. Higher Japanese yields have not translated into a stronger yen, as rising JPY rates largely reflect an inflation risk premium driven by fiscal concerns and perceptions that monetary policy remains behind the curve. As a result, Japan's real yields remain insufficiently attractive relative to rising US real yields.

We would need to see the BOJ tighten policy beyond what is already priced into markets before becoming more constructive on the yen. Until then, yield differentials and relative real-rate dynamics are likely to continue favouring the USDJPY, even if intervention risk acts as a constraint on further upside.

Asia ex-Japan (AXJ) currencies

The backdrop for AXJ currencies in 2H2026 remains cautious. Hawkish Fed rhetoric and periods of USD strength are likely to keep regional currencies on the defensive in the near term. The decline in oil prices to below US$80/barrel is supportive, particularly for net oil importers, but it does not fully alleviate underlying pressures.

Market sentiment is also likely to remain somewhat fragile, with geopolitical flare-ups posing a key risk that could quickly reverse the recent improvement in the oil outlook. Against this backdrop, we do not view the outlook for AXJ currencies as uniformly bearish, but neither do we believe the region is fully out of the woods.

Performance across Asian currencies is likely to remain highly differentiated, reflecting varying degrees of sensitivity to oil prices, differences in external balances and domestic policy credibility, as well as the extent of equity-flow support and exposure to USD and interest-rate dynamics.

Renminbi (RMB)

The offshore Chinese yuan (CNH) is likely to remain guided by the PBOC’s fixing bias, with policymakers still appearing comfortable with a gradual pace of RMB appreciation. In the near term, however, the CNH may have lost some of its earlier appreciation momentum, with USDCNH rebounding toward the 6.80 area as renewed USD strength and hawkish Fed repricing weigh on regional currencies.

We view this as a short-term adjustment to broader market dynamics and an effort to moderate the pace of appreciation, rather than a reversal of the underlying trend. Nonetheless, if China’s growth momentum continues to soften, investors may increasingly question whether the RMB’s relative outperformance remains fundamentally justified. In that scenario, maintaining RMB strength could become more challenging, particularly if domestic economic concerns begin to outweigh external drivers.

Singapore Dollar (SGD)

The SGD should continue to outperform many regional peers, supported by its lower-beta characteristics and the MAS's relatively tighter policy stance. That said, it is not insulated from broader USD strength, rising US Treasury yields, or weaker regional risk sentiment. As such, there may be scope for USDSGD to move higher in the near term if the USD remains firm and US yields continue to rise.

The upcoming MAS policy decision later this month will be a key focus. We see room for the MAS to remain on hold. Core CPI readings for April and May came in softer than expected, while the sharp decline in energy prices has further eased inflationary pressures. In addition, the pre-emptive tightening undertaken in April may already be sufficient to keep inflation on a moderating path, reducing the need for further policy action unless price pressures re-accelerate materially.

Ringgit (MYR)

We have turned neutral to slightly cautious on the MYR. While the macroeconomic story remains intact, much of the earlier fundamental re-rating now appears to be reflected in valuations. Domestic political developments, including state election-related noise, could introduce a modest risk premium in the near term. At the same time, the MYR is not immune to a stronger USD and a higher-for-longer US rate environment.

That said, downside risks should be partly mitigated by Bank Negara Malaysia’s efforts to encourage currency inflows and support onshore market liquidity. These measures should help cushion the MYR against bouts of external volatility, even as global factors remain the primary driver of near-term price action.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

The information provided herein may contain projections or other forward looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. Investments are subject to investment risks, including the possible loss of the principal amount invested.

The Bank, its related companies, their respective directors and/or employees (collectively “Related Persons”) may or might have in the future interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. The Bank and its Related Persons may also be related to, and receive fees from, providers of such investment products.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent. The contents are a summary of the investment ideas and recommendations set out in Bank of Singapore and OCBC Bank reports. Please refer to the respective research report for the interest that the entity might have in the investment products and/or issuers of the securities.

Investments are subject to investment risks, including the possible loss of the principal amount invested. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

This document may be translated into the Chinese language. If there is any difference between the English and Chinese versions, the English version will apply.

Foreign Currency disclaimer

- Foreign currency investments or deposits are subject to inherent exchange rate fluctuation that may provide opportunities and risks. Consequently, exchange rate fluctuations may affect the value of your foreign currency investments or deposits.

- Earning on foreign currency investments or deposits may change depending on the exchange rates prevalent at the time of their maturity if you choose to convert.

- Exchange controls may apply to certain foreign currencies from time to time.

- Any pre-termination costs will be taken and deducted from your deposit directly and without notice.

Cross-Border Marketing Disclaimers

OCBC Bank's cross border marketing disclaimers relevant for your country of residence.

Collective Investment Schemes

- A copy of the prospectus of each fund is available and may be obtained from the fund manager or any of its approved distributors. Potential investors should read the prospectus for details on the relevant fund before deciding whether to subscribe for, or purchase units in the fund.

- The value of the units in the funds and the income accruing to the units, if any, may fall or rise. Please refer to the prospectus of the relevant fund for the name of the fund manager and the investment objectives of the fund.

- Investment involves risks. Past performance figures do not reflect future performance.

- Any reference to a company, financial product or asset class is used for illustrative purposes and does not represent our recommendation in any way.

- For funds that are listed on an approved exchange, investors cannot redeem their units of those funds with the manager or may only redeem units with the manager under certain specified conditions. The listing of the units of those funds on any approved exchange does not guarantee a liquid market for the units.

- The indicative distribution rate may not be achieved and is not an indication, forecast, or projection of the future performance of the Fund.

Any opinions or views of third parties expressed in this document are those of the third parties identified, and do not represent views of Oversea-Chinese Banking Corporation Limited (“OCBC Bank”, “us”, “we” or “our”).