Global Outlook

May 2026

Global growth shows resilience

Growth momentum remained strong in 1Q2026, but the prolonged Middle East conflict has increased the risk of stagflation in the global economy.

Selena Ling

Chief Economist & Head,

OCBC Group Research,

OCBC

April proved resilient despite the prolonged Iran war and the failure to reopen the Strait of Hormuz. Major central banks (Federal Reserve, European Central Bank, Bank of England, Bank of Japan) stayed on hold, though policy divergence widened. The Federal Open Market Committee (FOMC) – the branch of the Federal Reserve that determines monetary policy – leaned hawkish. BOJ divisions grew, and currency volatility intensified as USDJPY breached 160, prompting intervention. Global equities advanced, with the MSCI All Country World Index reaching a new record high. US 10-year Treasury yields tested 4.4% amid persistent inflation and elevated energy prices. UAE’s withdrawal from OPEC+ led to a modest June production hike.

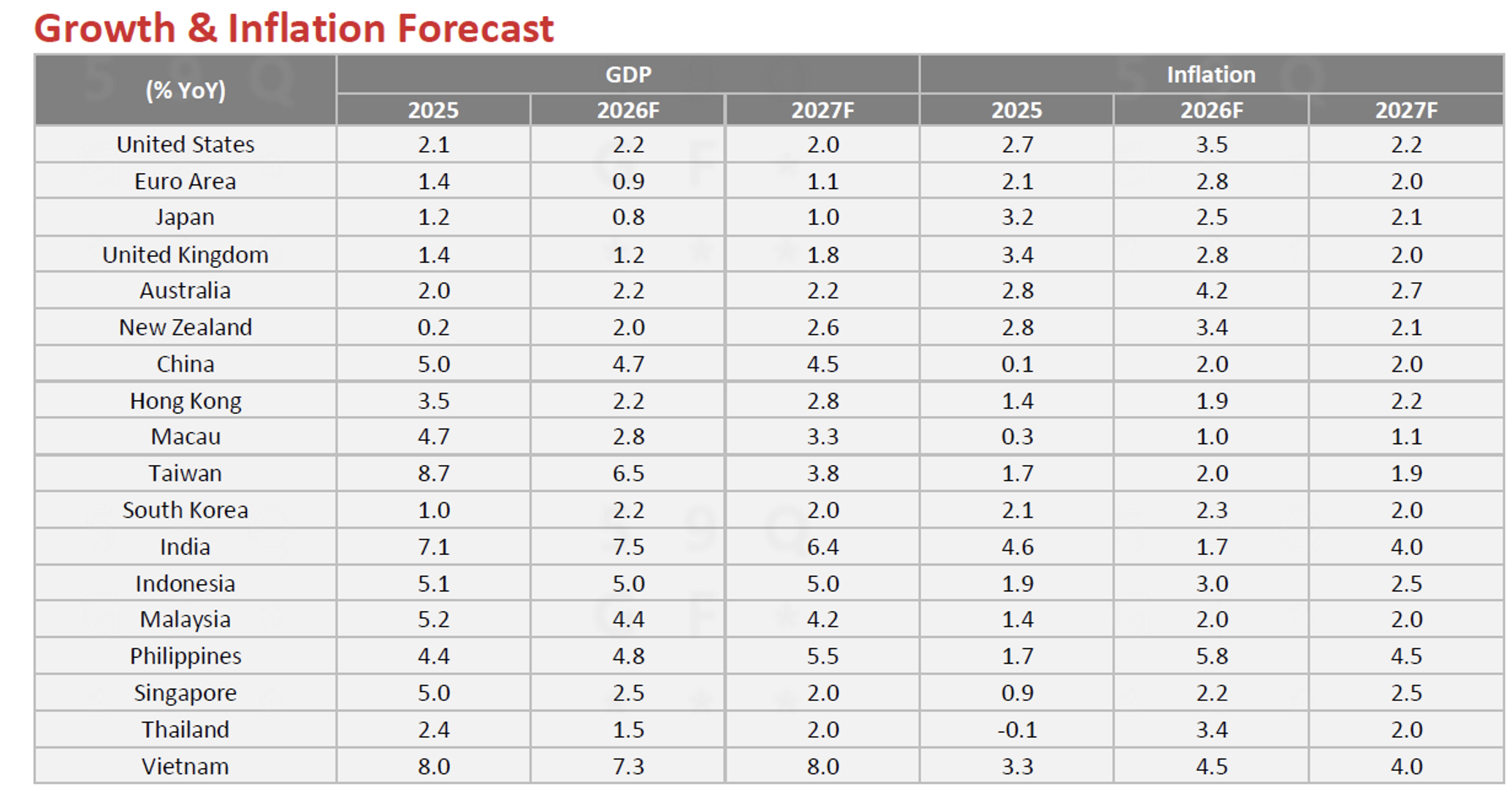

Asia’s 1Q2026 growth remained resilient due to supply-chain diversification and AI investment, though rising cost pressures are emerging. ASEAN governments rolled out energy-saving and fiscal measures. Looking ahead, markets will focus on US economic and employment data, leadership under new FOMC Chair Kevin Warsh, and whether risk assets can sustain gains amid a tighter liquidity regime.

China’s growth reaccelerated to 5% YoY, supported by policy easing and manufacturing re-rating, positioning it as a potential long-term beneficiary despite energy-related risks from the Iran war.

United States

We remain comfortable with our 2026 US growth forecast of 2.2% despite rising stagflation risks. Our baseline assumes continued resilience in global growth driven by five factors. First, investment and production linked to artificial intelligence remain robust. Second, effective US tariff rates have declined meaningfully following the Supreme Court ruling. Third, growth momentum from 2H2025 has carried into early 2026. Fourth, fiscal and financial conditions remain broadly supportive. Fifth, businesses have repeatedly demonstrated adaptability to geopolitical disruptions and supply side shocks in recent years.

US economic data have reinforced this outlook. 1Q2026 GDP rebounded to a 2.0% annualised pace, supported by stronger investment, exports, consumption and government spending, though higher imports continued to weigh on growth.

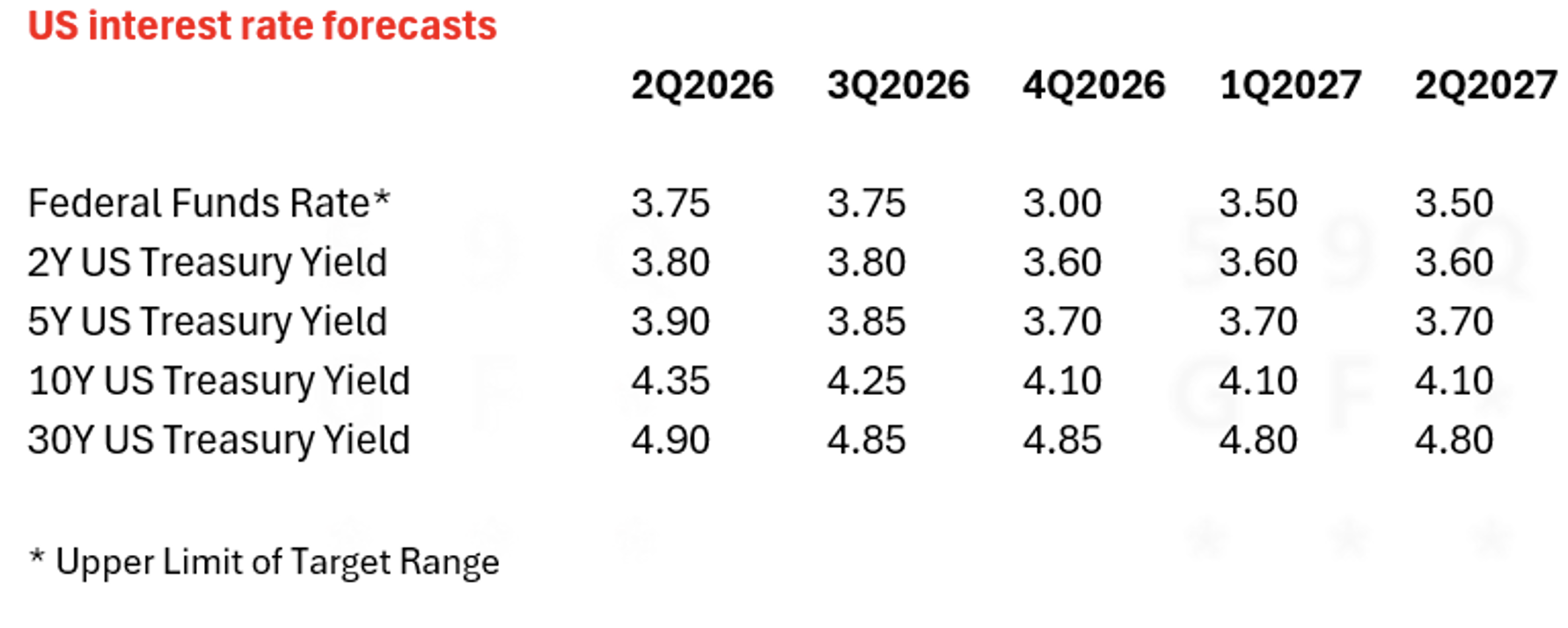

Overall, US assets were supported by resilient growth and strong AI related earnings, while higher oil prices and renewed inflation risks kept US Treasury yields and the US Dollar firm. The Fed kept rates unchanged at 3.50%–3.75% in April, with the FOMC leaning modestly hawkish as three members opposed maintaining the easing bias.

Euro-Area

We maintain our 2026 GDP growth forecast at 0.9% and have revised headline CPI higher to 2.8% from 2.5% YoY, reflecting the impact of ongoing Middle East tensions. Higher oil, gas and fertiliser prices are feeding through to broader inflation, particularly food costs. ECB President Christine Lagarde highlighted the “double uncertainty” around the duration of the oil shock and the extent of price pass through, while reaffirming the ECB’s commitment to price stability. We do not expect an aggressive tightening cycle and continue to pencil in a 25bp insurance hike in June.

The ECB’s latest Consumer Expectations Survey signals mounting stagflation risks. One year inflation expectations jumped to 4.0% from 2.5%, while three-year expectations rose to 3.0%. Economic confidence fell sharply to 93.0 in April, alongside weaker industrial sentiment. In response, the European Commission proposed the AccelerateEU temporary state aid framework and coordinated oil stock releases with the IEA to help cushion price pressures.

Japan

Japan’s economy ended 2025 on a softer footing, with 4Q2025 GDP growing just 0.1% QoQ, undershooting expectations and highlighting weak domestic demand. Full‑year growth recovered to 1.1% in 2025 from a contraction in 2024, but macro uncertainty persists into 2026. The BOJ cut its growth forecast to 0.5% while sharply raising its core CPI outlook to 2.8%, reflecting rising inflation risks. We now expect a 25bp rate hike at the June meeting after the BOJ held policy steady at 0.75% in April, despite dissent from three board members – a hawkish hold. March factory output declined 0.5% MoM and core CPI rose 1.8% YoY. The combination of weakening growth and rising inflation points to an increasingly stagflationary backdrop, complicating policy normalisation. Fiscal policy remains supportive but cautious, with a record FY2026 budget and no additional stimulus planned.

China

China has lowered its 2026 GDP growth target to a range of 4.5%–5% from “around 5%”, with the lower bound likely representing the minimum rate needed to stay on track toward the 2035 goal of doubling per capita GDP versus 2020 levels. We keep our 2026 growth forecast unchanged at 4.7% despite the escalating Iran war. Consumption recovery remains uneven due to slowing income growth and weak household appetite for leverage, with growth expected to moderate to around 4.8% in 2Q2026.

The economy remains broadly on track to meet the official target. Moody’s revised China’s sovereign outlook to “stable” from “negative,” citing resilience to domestic, trade and geopolitical headwinds. This shift reflects China’s demonstrated ability to absorb external shocks and reinforces the continued re‑rating of its manufacturing depth and supply‑chain resilience amid global uncertainty.

Source: OCBC Group Research

Source: OCBC Group Research

The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

The information provided herein may contain projections or other forward looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. Investments are subject to investment risks, including the possible loss of the principal amount invested.

The Bank, its related companies, their respective directors and/or employees (collectively “Related Persons”) may or might have in the future interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. The Bank and its Related Persons may also be related to, and receive fees from, providers of such investment products.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent. The contents are a summary of the investment ideas and recommendations set out in Bank of Singapore and OCBC Bank reports. Please refer to the respective research report for the interest that the entity might have in the investment products and/or issuers of the securities.

Investments are subject to investment risks, including the possible loss of the principal amount invested. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

This document may be translated into the Chinese language. If there is any difference between the English and Chinese versions, the English version will apply.

Cross-Border Marketing Disclaimers

OCBC Bank's cross border marketing disclaimers relevant for your country of residence.

Any opinions or views of third parties expressed in this document are those of the third parties identified, and do not represent views of Oversea-Chinese Banking Corporation Limited (“OCBC Bank”, “us”, “we” or “our”).