Global Outlook

December 2020

New Hope in the New Year

The new year is likely to bring new hope to the world economy. The macroeconomic outlook will favour financial markets as global growth rebounds strongly in 2021, new vaccines prevent fresh virus waves, central banks remain dovish, political risks ease in the US, Europe and Asia, government bond yields stay low and the US Dollar continues to weaken to the benefit of risk assets.

A strongly reflationary outlook

Following the worst shock to the global economy since the 1930s Great Depression, the Covid-19 pandemic and resulting lockdowns in 2020 are set to give way to a strongly reflationary environment in 2021.

There are still several near-term risks to navigate before this year ends. The US, UK, Eurozone and Japan are suffering second or third virus waves. In addition, the European Union and the UK must agree to a fresh trade treaty before the end of December to avoid a chaotic “no deal” exit when their current trading arrangements expire as 2020 finishes. Last, President Donald Trump has yet to concede the US election.

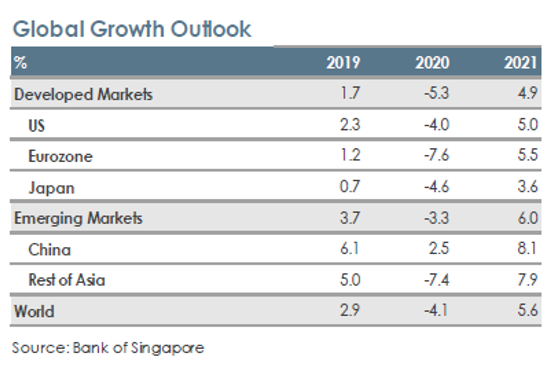

Strong economic rebound in 2021

Despite risks, forward-looking financial markets are likely to discount near term threats and focus instead on the favourable longer-term outlook for risk assets in 2021.

First, the global economy is set to rebound strongly in the new year as the distribution of vaccines allows consumers to spend freely again, releasing pent up demand from this year’s lockdowns.

We project the world economy to expand by 5.6% in 2021 after contracting by -4.1% in 2020. This would be a much faster pace of growth than the 3.5% average annual rate achieved by the world economy over the last five decades.

Further, the global recovery is likely to be broad-based. We forecast China to keep leading the rebound with GDP set to grow by 8.1% in 2021 after a likely 2.5% expansion in 2020.

Similarly, we see other emerging economies in Asia rebounding by 7.9% next year, compared to a likely steep contraction of -7.4% this year.

Developed market economies are also likely to experience strong growth in 2021. We forecast the US, Eurozone, Japan and the UK to expand by 5.0%, 5.5%, 3.6% and 4.7% respectively.

Financial markets face further uncertainty. The US elections have now passed but vote counts in several states are being challenged in the courts. In addition, the US, UK and Eurozone are suffering new virus waves.

But once the US electoral results are clear, financial markets are likely to focus again on the favourable outlook for risk assets underpinned by the global recovery, upcoming vaccines, very dovish central banks, low government bond yields and a weaker US Dollar.

Positive developments with vaccines

Second, the development of viable vaccines will prevent fresh virus waves over the next few quarters.

Already, governments have become more effective at managing new virus waves even before the widespread distribution of upcoming vaccines begins in 2021.

During the first lockdowns in the spring of 2020, economic activity plummeted as schools, factories, offices, restaurants and leisure venues were all closed. But in the second lockdowns occurring now, governments in the US, Europe and Japan have restricted gyms, sporting events, indoor dining and other entertainment but have allowed schools, factories and some offices to stay open.

The purchasing manager index (PMI) – an indicator of economic activity that signals contraction for readings below 50.0 and expansion for prints above 50.0 – shows that composite PMI has fallen sharply again in 4Q 2020 for the UK and Eurozone. But the monthly PMI surveys are nowhere near as weak as they were during 2Q 2020.

In 2021, viable vaccines should reduce the outbreak of fresh virus waves and governments will be more experienced in limiting the adverse impact on economic activity.

Central banks could add monetary stimulus

Third, central banks are set to remain very dovish and are likely to add further monetary stimulus — if needed — to support economic recovery.

The Federal Reserve may increase its current pace of bond buying from US$80 billion a month of US Treasuries and US$40 billion of mortgage-backed securities if the US economy suffers from America’s current virus waves.

Moreover, even if the Fed does not expand its quantitative easing any further, the central bank is likely to keep its Fed funds interest rate unchanged at 0.00-0.25% until as late as 2024 or 2025.

Inflation – as measured by changes in core personal consumption expenditure prices (PCE) – remains well below the Fed’s 2% goal at just 1.4% YoY for October. We expect that core PCE inflation may not recover to average 2% for several years given the shock from the pandemic.

Thus, the Fed, having shifted to a new strategy of average inflation targeting in August this year to achieve inflation of around 2% over time, appears unlikely to start hiking its Fed funds rate before 2024 or 2025.

Similarly, the European Central Bank (ECB) also seems likely to add further monetary stimulus. The ECB has already signalled it is willing to expand its €1.35 trillion Pandemic Emergency Purchase Programme (PEPP) given core inflation is currently just above zero percent in the Eurozone.

We expect the central bank will announce at its last meeting of the year in December that it will increase its planned bond purchases by another €500 billion and keep its quantitative easing in place throughout 2021.

Political risks have receded

Fourth, political risks appear set to recede in 2021. The EU and UK remain likely to agree to a trade deal before the end of 2020; President-elect Joe Biden will move into the White House in January and the new US government is unlikely to raise tariffs further on imports from China, Europe, Mexico and Canada, marking a clear break with the unpredictable trade policies of the Trump administration.

Interest rates to stay very low for next few years

Fifth, government bond yields are likely to stay at very low levels despite the global economy’s rebound in 2021. The improving economic outlook has resulted in our projections for longer term US Treasury yields and swap rates being revised upwards, while our forecasts for shorter term bond yields have stayed largely unchanged.

Thus, we now expect 10Y and 30Y US Treasury yields to rise to 1.20% and 2.15% respectively over the next year after hitting our earlier long-term forecasts of 0.90% and 1.75%. But we still project government bond yields to stay at historically low levels overall, given that the Federal Reserve will not raise interest rates until the middle of the decade, and inflation will likely stay below the central bank’s 2% target on average over the next few years.

US Dollar looks set to keep weakening

Last, the US Dollar is set to keep weakening in 2021 as risk-seeking investors reduce demand for the safe-haven greenback and the Fed keeps interest rates at current near zero levels to push inflation back to a 2% average rate.

Overall favourable macro outlook

The global economy’s rebound in 2021 will contrast strongly with the major shock suffered during the pandemic in 2020.

Thus, the overall macroeconomic outlook – rebounding growth, potentially less political risk, a weaker US Dollar, low bond yields and dovish central banks – continues to favour risk assets despite renewed virus waves as 2020 ends.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

The information provided herein may contain projections or other forward looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. Investments are subject to investment risks, including the possible loss of the principal amount invested.

The Bank, its related companies, their respective directors and/or employees (collectively “Related Persons”) may or might have in the future interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. The Bank and its Related Persons may also be related to, and receive fees from, providers of such investment products.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent. The contents are a summary of the investment ideas and recommendations set out in Bank of Singapore and OCBC Bank reports. Please refer to the respective research report for the interest that the entity might have in the investment products and/or issuers of the securities.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Cross-Border Marketing Disclaimers

Please click here for OCBC Bank's cross border marketing disclaimers relevant for your country of residence.