Proyeksi Global

July 2026

Growth likely to remain resilient

US growth has remained surprisingly resilient, supported by strong AI-related investment and the unwinding of Liberation Day tariffs.

Selena Ling

Chief Economist & Head,

OCBC Group Research,

OCBC

Geopolitical risk premiums have eased following the US-Iran MOU, helping lower crude oil prices as maritime traffic through the Strait of Hormuz gradually normalises. However, negotiations remain fragile, and risks persist.

Elsewhere, markets have been shaped by hawkish Fed repricing, with futures now fully pricing in a 25bp rate hike by year-end as Fed Chair Kevin Warsh retreats from forward guidance.

Concerns over AI valuations and capex sustainability have also added to volatility. Despite this, US equities recorded their strongest quarterly gain in six years.

Meanwhile, USDJPY touched a four-decade high as interest-rate differentials became a less reliable driver of the exchange rate, keeping intervention risks in focus. Longer term, reserve managers are expected to gradually diversify away from the US dollar towards the Euro, Yuan and Gold, according to the Official Monetary and Financial Institutions Forum (OMFIF).

It remains unclear whether policymakers will look through the 2Q2026 energy-price shock, which is still feeding through to a broader range of goods and services. Inflation may not peak until 3Q2026. At the same time, growth has remained surprisingly resilient, supported by strong AI-related investment and the unwinding of Liberation Day tariffs.

United States

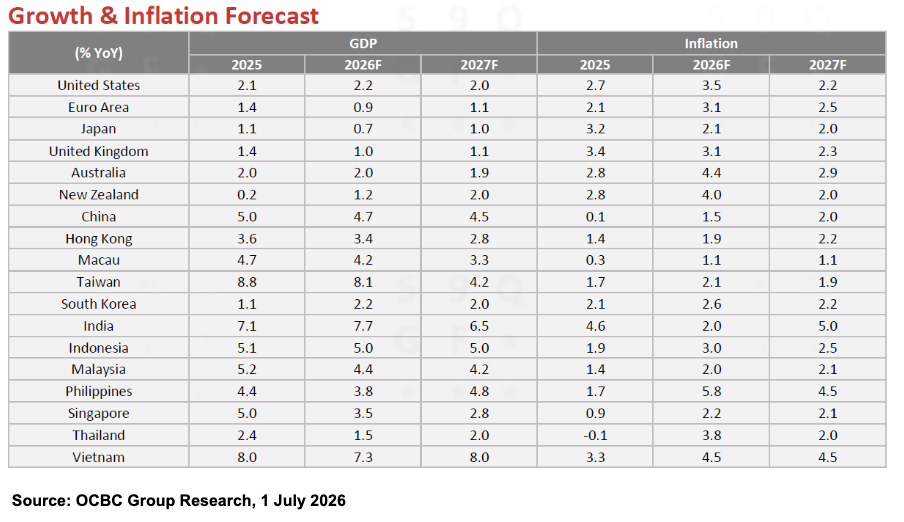

We maintain our 2026 growth forecast at 2.2%, with growth expected to rebound to above 3% QoQ in 2Q2026 from 2.1% in 1Q2026, driven by a recovery in net exports.

We expect inflation to peak in 2Q2026 before moderating in 2H2026, supported by fading energy-related effects and a decline in the oil risk premium. Our 2026 inflation forecast remains at 3.5% YoY, up from 2.7% in 2025.

Following the FOMC meeting, markets briefly priced in earlier rate hikes, pushing Treasury yields higher. However, a sharp decline in oil prices to pre-war levels by end-June eased inflation concerns, leading investors to partially reverse the move.

New Fed Chair Kevin Warsh has also launched a strategic review of the Federal Reserve’s operating framework, covering communications, balance sheet policy, data methodology, the inflation framework, and labour-market assessment, with completion targeted for end-2026. Reduced reliance on forward guidance could increase market uncertainty.

Euro-Area

The euro area outlook has weakened following the Middle East conflict, with growth expected to slow to 0.9% YoY in 2026 from 1.4% in 2025. Our forecast, unchanged for some time, is now aligned with the European Commission’s Spring Economic Forecast after its downward revision in May.

The impact on the labour market has been limited so far, with unemployment holding steady at 6.3% in April 2026. However, inflation remains the European Central Bank’s primary concern as policymakers continue to highlight persistent pipeline price pressures. Headline CPI rose to 3.2% YoY in May from 3.0% in April, prompting us to raise our 2026 inflation forecast to 3.1% from 2.8%, mainly due to higher energy prices.

Following the 25bp rate hike in June, we expect the ECB to deliver one additional 25bp hike in September, taking the deposit rate to 2.5%.

Japan

The BOJ raised its policy rate from 0.75% to 1.00% at its June meeting, in line with expectations. Inflation continued to firm, with Tokyo core CPI rising to 1.6% YoY in June from 1.3% in May, although it remained below the BOJ’s 2% target for a fifth straight month. Core-core inflation (excluding fresh food and energy) increased to 1.9% YoY from 1.6%, pointing to a broader pass-through of higher energy costs.

Domestic demand remains resilient. Retail sales grew 5.3% YoY in May, up from a revised 2.8% in April and well above expectations, supported by strong wage growth and government subsidies.

Against this backdrop, we maintain our 2026 GDP growth forecast at 0.8% and headline CPI forecast at 2.5%.

China

Recent data point to a further slowdown in China’s growth momentum. While high-tech manufacturing and AI-related sectors continue to support activity, weakness in consumption, the property sector, manufacturing investment, and infrastructure spending suggests the broader economy remains under pressure.

We expect GDP growth to moderate to around 4.5% YoY in 2Q2026, reflecting China’s ongoing K-shaped recovery. Nevertheless, the economy remains broadly on track to meet the official 4.5–5.0% growth target, and we maintain our 2026 growth forecast at 4.7%.

Rates

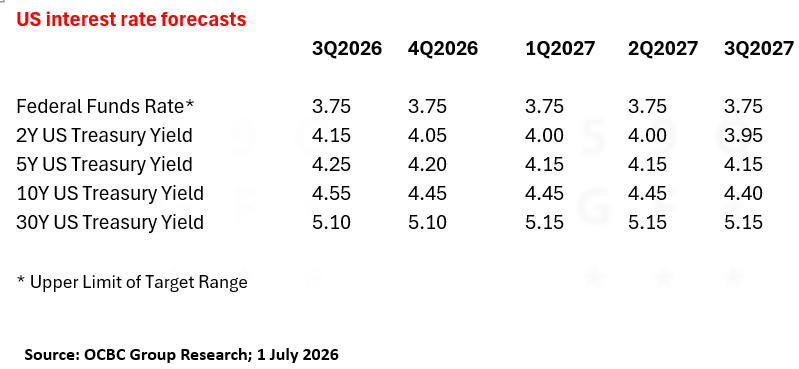

Fed funds futures turned more hawkish following the June dot plot, with nine FOMC members signalling at least one rate hike before year-end. Market pricing has remained hawkish despite lower oil prices and benign May PCE inflation data. We continue to expect the Fed to keep rates unchanged at 3.50 – 3.75% through 2026, although the risk of a hike remains. This tightening risk is likely to keep short-dated Treasury yields relatively elevated, even if any additional hike is eventually followed by rate cuts in 2027.

We expect the BOE to keep its Bank Rate unchanged at 3.75% through 2026, given its already restrictive stance and soft growth outlook. Governor Andrew Bailey struck a balanced tone at the June MPC meeting, noting that bringing inflation back to target too quickly could create unnecessary volatility in growth. While two MPC members voted for a rate hike as a risk-management measure, their stance appeared cautious rather than conviction-driven. Meanwhile, weakening demand and labour market conditions should help limit second-round inflation pressures. Reflecting this backdrop, market expectations for further tightening have eased significantly.

We expect the ECB to deliver one additional 25bp rate hike in 3Q2026, as inflation is likely to remain above target through most of 2027. However, we do not foresee a more aggressive tightening cycle. The ECB has signalled that the current inflation shock is significant but not persistent enough to warrant a stronger policy response, supporting a measured and gradual approach to further rate increases.

The June Reserve Bank of Australia meeting minutes and current economic conditions support our view that the cash rate will remain at 4.35% through 2026. The Reserve Bank of Australia continues to adopt a wait-and-see approach, noting that it will take time to assess the full impact of past policy tightening on the economy. Consistent with this cautious stance, markets are pricing in only a modest chance of a further hike, with cash rate futures implying around 11bps of tightening by year-end.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

The information provided herein may contain projections or other forward looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. Investments are subject to investment risks, including the possible loss of the principal amount invested.

The Bank, its related companies, their respective directors and/or employees (collectively “Related Persons”) may or might have in the future interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. The Bank and its Related Persons may also be related to, and receive fees from, providers of such investment products.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent. The contents are a summary of the investment ideas and recommendations set out in Bank of Singapore and OCBC Bank reports. Please refer to the respective research report for the interest that the entity might have in the investment products and/or issuers of the securities.

Investments are subject to investment risks, including the possible loss of the principal amount invested. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

This document may be translated into the Chinese language. If there is any difference between the English and Chinese versions, the English version will apply.

Cross-Border Marketing Disclaimers

OCBC Bank's cross border marketing disclaimers relevant for your country of residence.

Any opinions or views of third parties expressed in this document are those of the third parties identified, and do not represent views of Oversea-Chinese Banking Corporation Limited (“OCBC Bank”, “us”, “we” or “our”).