The U.S. Dollar is a clear beneficiary of Mr Trump’s victory for three reasons:

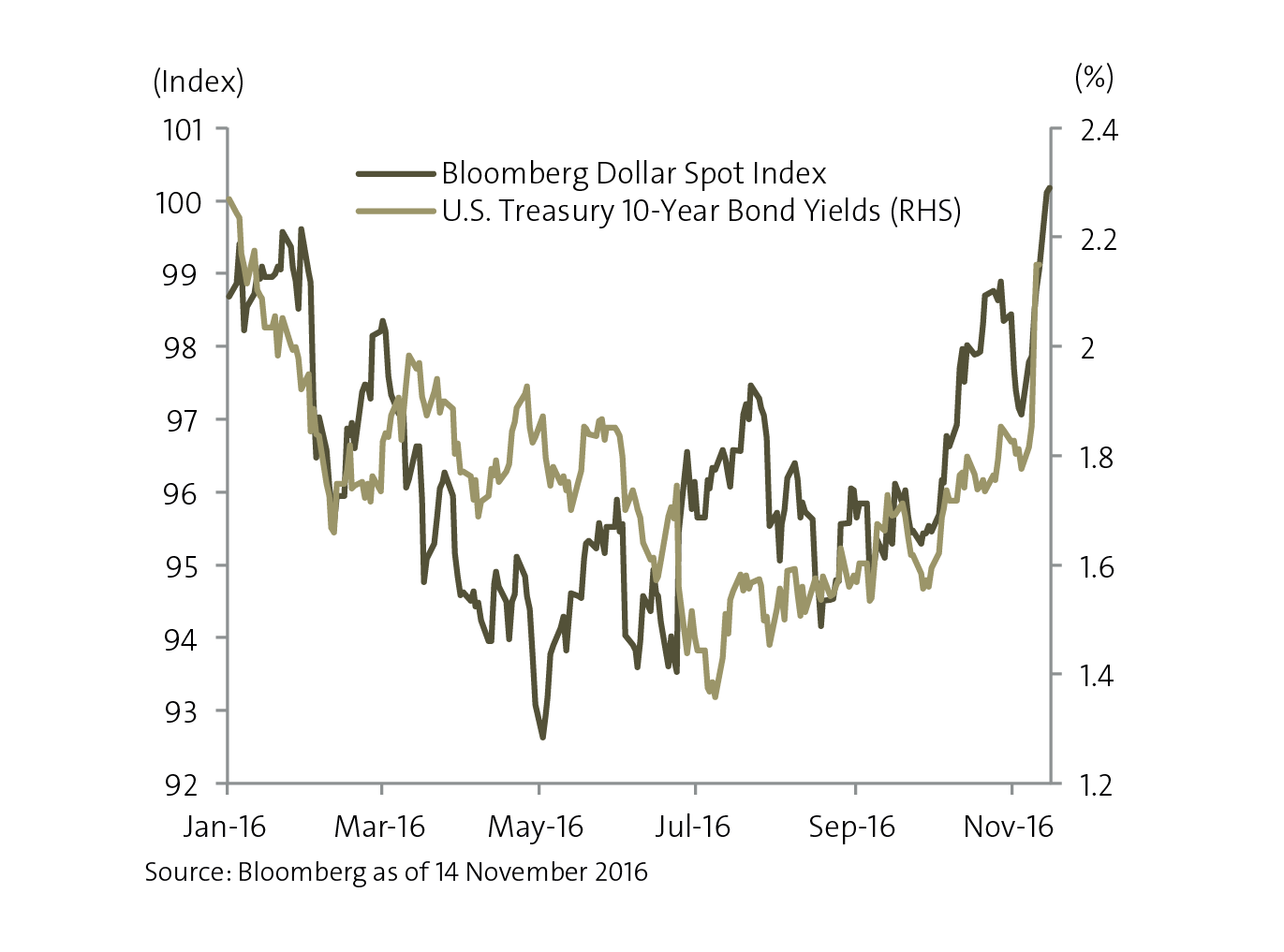

Chart 1: U.S. Dollar and 10-Year Treasury yields enjoy a boost post-election

First, President Trump, supported by a Republican House and Senate, will likely implement more expansionary fiscal policy which is pro-growth and could encourage the Fed to hike interest rates at a faster pace than planned and exert upward pressure on U.S. Treasury yields. Fiscal irresponsibility that boost U.S. growth will likely mean stronger U.S. Dollar ahead.

Second, Trump’s tax reform proposals to encourage corporate profits repatriation to fund infrastructure spending plans would be U.S. Dollar-positive.

A temporary reduction in the tax rate on repatriated earnings would likely have a similar impact of boosting the U.S. Dollar as the Homeland Investment Act (HIA) had in 2005. The extent of gains would depend on whether the foreign cash is already in U.S. Dollar or not.

Third, the shock of Brexit and now a Trump victory could fan concerns over European political outlook, which is EUR negative at least against the U.S. Dollar. Brexit and Trump’s election highlights a global trend towards populism and nationalism, which could lead to the break up of the Eurozone. Pro-EU parties are likely now more worried ahead of the 4 December Italian constitutional referendum and Dutch, French and German elections in 2017 (by March, May and September, respectively).

Political and economic uncertainty ahead strengthens the case for holding gold in a portfolio as a diversifier. But possible changes in fiscal policy that have pushed U.S. Treasury yields higher would offset safe haven demand and temper gold’s upside.

We expect gold prices to trade in a wider range of $1230-$1380/oz on a 3-6 month timeframe.

Potential trade conflicts and risks of higher U.S. interest rates are a negative medium-term combination for EM currencies and the Canadian Dollar.

Within EM, this concern extends beyond the Mexican Peso, which has been the most prominently vulnerable currency. Wariness will likely increasingly pervade the currencies of many of the U.S. trading partners in EM Asia, most obviously China and Korea.

Beyond the drag on trade-exposed EM currencies, risk of higher U.S. interest rates could trigger bond market outflows from EM. This would make EM carry trade less rewarding, even for the ‘good’ carry currencies such as the IDR, INR, RUB and BRL.

Important Information

The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person.

Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

A copy of the prospectus of each fund is available and may be obtained from the relevant fund manager or any of its approved distributors. Potential investors should read the prospectus for details on the relevant fund before deciding whether to subscribe for, or purchase units in the fund. The value of the units in the funds and the income accruing to the units, if any, may fall or rise. Please refer to the prospectus of the relevant fund for the name of the fund manager and the investment objectives of the fund.

The information provided herein may contain projections or other forward looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same.

OCBC Bank, OCBC Investment Research Private Limited, OCBC Securities Private Limited, Bank of Singapore and their respective associated and connected corporations together with their respective directors and officers may have or take positions in any securities mentioned in this report and may also perform or seek to perform broking and other investment or securities related services for the corporations whose securities are mentioned in this report as well as other parties generally.

Foreign currency investments or deposits are subject to inherent exchange rate fluctuation that may provide opportunities and risks. Earnings on foreign currency investments or deposits would be dependent on the exchange rates prevalent at the time of their maturity if any conversion takes place. Exchange controls may be applicable from time to time to certain foreign currencies. Any pre-termination costs will be deducted from your deposit.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such. The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent.

Cross-Border Disclaimer

1. Indonesia: The offering of the investment product in reliance of this document is not registered under the Indonesian Capital Market Law and its implementing regulations, and is not intended to constitute a public offering of securities under the Indonesian Capital Market Law and its implementing regulations. The investment product may not be offered or sold, directly or indirectly, within Indonesia or to citizens (wherever they are domiciled or located), entities or residents, in any manner which constitutes a public offering of securities under the Indonesian Capital Market Law and its implementing regulations. 2. Malaysia: Oversea-Chinese Banking Corporation Limited ("OCBC Bank") does not hold any licence, registration or approval to carry on any regulated business in Malaysia (including but not limited to any businesses regulated under the Capital Markets & Services Act 2007 of Malaysia), nor does it hold itself out as carrying on or purport to carry on any such business in Malaysia. Any services provided by OCBC Bank to residents of Malaysia are provided solely on an offshore basis from outside Malaysia, either as a result of “reverse enquiry” on the part of the Malaysian residents or where OCBC Bank has been retained outside Malaysia to provide such services. As an integral part of the provision of such services from outside Malaysia, OCBC Bank may from time to time make available to such residents documents and information making reference to capital markets products (for example, in connection with the provision of fund management or investment advisory services outside of Malaysia). Nothing in such documents or information is intended to be construed as or constitute the making available of, or an offer or invitation to subscribe for or purchase any such capital markets product. 3. Myanmar: OCBC Bank does not hold any licence or registration under the FIML or other Myanmar legislation to carry on, nor do they purport to carry on, any regulated activity in Myanmar. All activities relating to the client are conducted strictly on an offshore basis. The customers shall ensure that it is their responsibility to comply with all applicable local laws before entering into discussion or contracts with the Bank. 4. Taiwan: The provision of the information and the offer of the service concerned herewith have not been and will not be registered with the Financial Supervisory Commission of Taiwan pursuant to relevant laws and regulations of Taiwan and may not be provided or offered in Taiwan or in circumstances which requires a prior registration or approval of the Financial Supervisory Commission of Taiwan. No person or entity in Taiwan has been authorised to provide the information and to offer the service in Taiwan. 5. Thailand: Please note that OCBC Bank does not maintain any licences, authorisations or registrations in Thailand nor is any of the material and information contained, or the relevant securities or products specified herein approved or registered in Thailand. Interests in the relevant securities or products may not be offered or sold within Thailand. The attached information has been provided at your request for informational purposes only and shall not be copied or redistributed to any other person without the prior consent of OCBC Bank or its relevant entities and in no way constitutes an offer, solicitation, advertisement or advice of, or in relation to, the relevant securities or products by OCBC Bank or any other entities in OCBC Bank’s group in Thailand. 6. Hong Kong SAR: This document is for information only and is not intended for anyone other than the recipient. It has not been reviewed by any regulatory authority in Hong Kong. It is not an offer or a solicitation to deal in any of the financial products referred to herein or to enter into any legal relations, nor an advice or a recommendation with respect to such financial products. It does not have regard to the specific investment objectives, financial situation and the particular needs of any recipient or Investor. This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without OCBC Bank’s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates to any registration, licensing or other requirements within such jurisdiction.

© Copyright 2016 - OCBC Bank | All Rights Reserved. Co. Reg. No.: 193200032W